Consumer Economy

- Auto/Light Truck Sales (ALTSALES) 16.1M +71.0K (+0.44% m/m)

- Nonfarm Payrolls (PAYEMS) 159.0M +172.0K (+0.11% m/m)

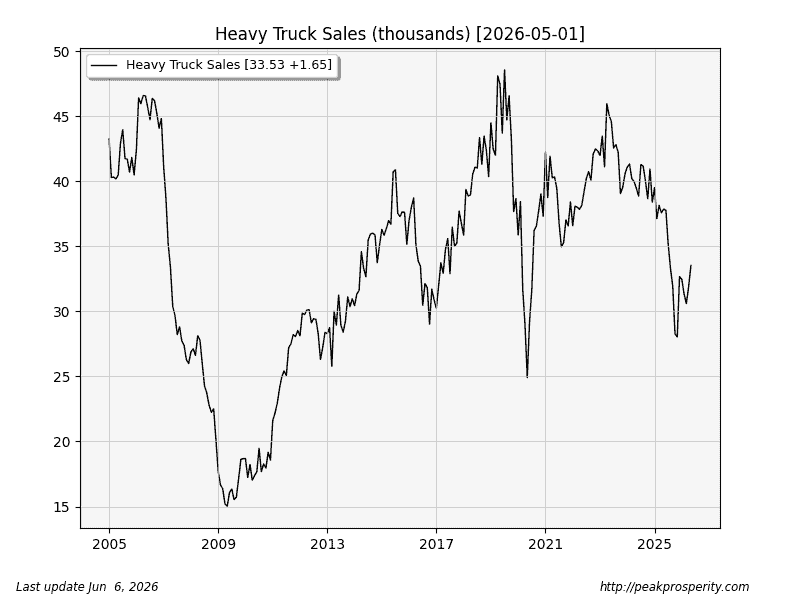

No significant changes in auto/light truck sales in May. Auto sales plunged to a new all-time low, but Americans stopped liking autos in 2014, and sales just keep moving lower. Recession-detector Heavy truck sales moved higher [+5.17%]. It has been recovering since late 2025. That’s not recessionary.

We saw stronger-than-expected payrolls this week; in the following table (link), you can see which sectors did best, although FRED provides raw numbers, not net change, so you have to do the math yourself.

Biggest changes: Government +52k, Health Care Services +47k (source – stlouisfed).

Note that revisions are now actually (modestly) increasing some previous payrolls estimates.

Payrolls release at 08:30 eastern on Friday seemed to cause a massive Metals Slammy, alongside a reverse-confetti operation in the dollar (a rally). More on that later.

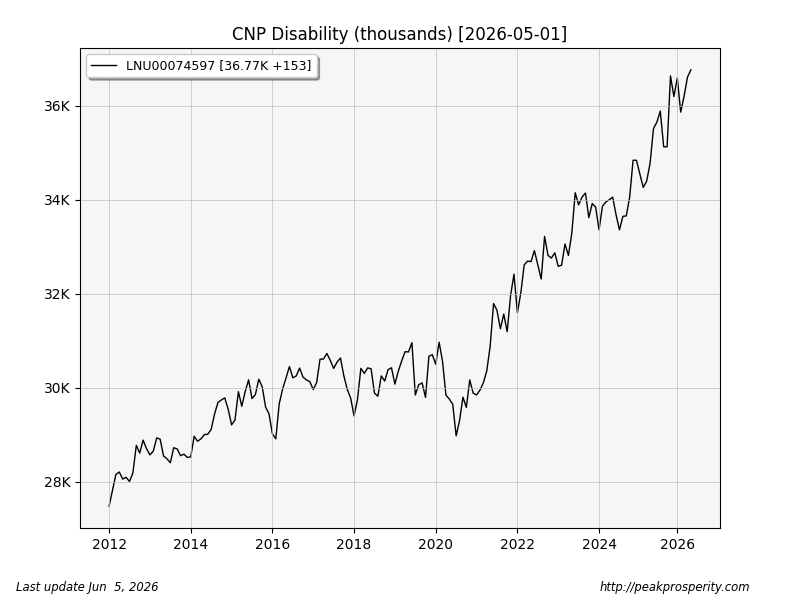

With a Disability

- CNP (LNU00074597) 36.76M +153k +0.42%

- CLF (LNU01074597) 8.79M +208k +2.42%

- EMP (LNU02074597) 7.99M +22k +0.28%

- NILF (LNU05074597) 27.98M -54k -0.19%

This month saw a new all-time high in total population disability (CNP); something mysterious continues to disable the population.

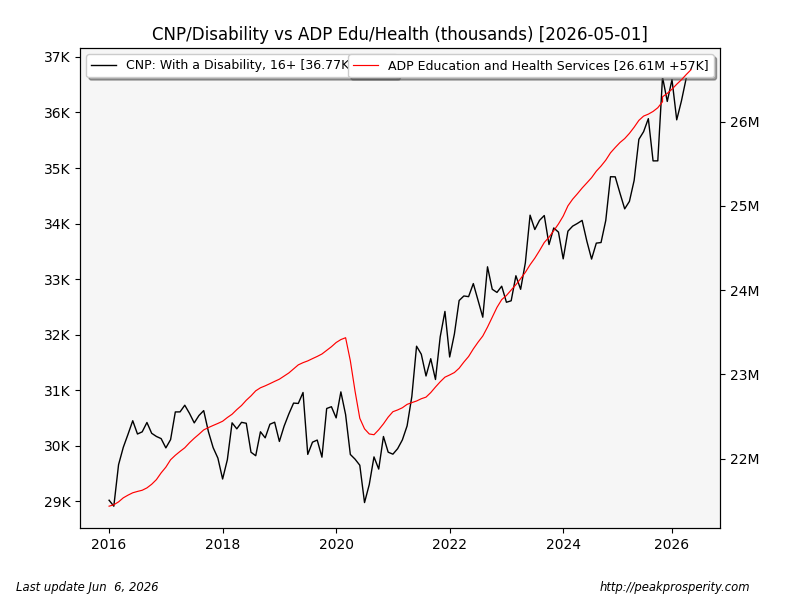

ADP confirms this month’s private payrolls change (+122k), the “education and health services” saw the largest increase at 57k. “AHS” is 20% of US employment, but it saw 50% of employment growth.

Here’s a combination of “population with a disability” alongside the AHS workforce over time. It is just a coincidence that AHS increases match up with the increase in CNP with a disability. The ratio is roughly 4 new sickcare workers for every 6 new people With a Disability.

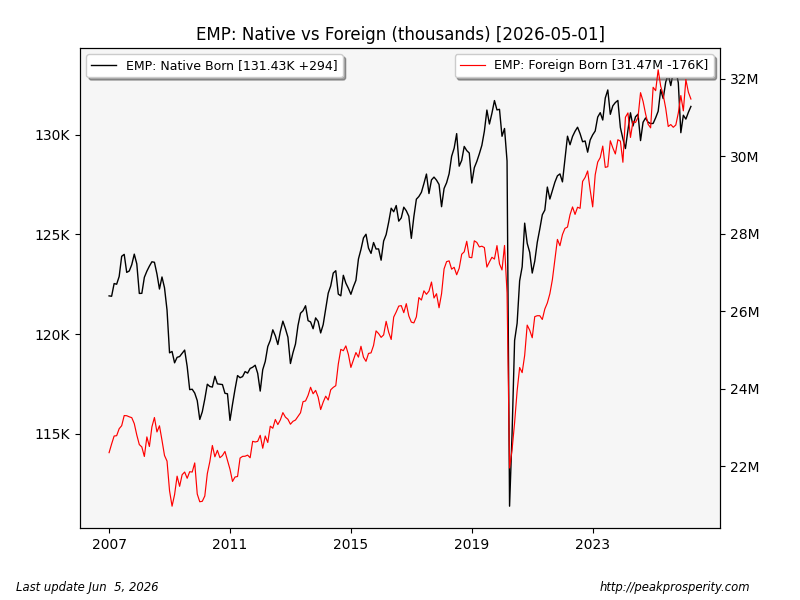

Employment: Native, Foreign

- Native Born (LNU02073413) 131.426M +294k +0.22%

- Foreign Born (LNU02073395) 31.472M -176k -0.56%

After spiking higher in March, foreign-born workers (red line) have fallen for the past two months, while native-born workers have gained jobs.

Credit & Rates

- Total Bank Credit (TOTBKCR) 19.58T +10.4B (+0.05% w/w)

- Fed Balance Sheet (WALCL) 6.71T +7.1B (+0.11% w/w)

- US 30 Year Mortgage Rate (MORTGAGE30US) 6.48% -5 bp

- 3-Month Treasury (DGS3MO) 3.72% +3 bp

- 1-Year Treasury (DGS1) 3.84% +5 bp

- 10-Year Treasury (DGS10) 4.52% +7 bp

- 20+ Treasury ETF (TLT.N) -0.82% w/w

There was a small increase in bank credit;

by mike-from-jersey

by mike-from-jersey