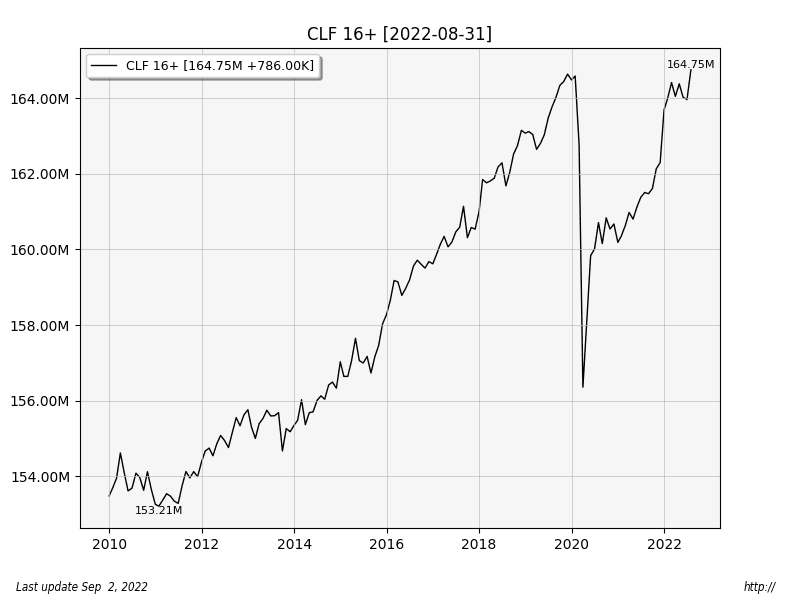

Payrolls came in reasonably strong on Friday; the headline number was +315,000, with the labor force growing by 786,000, a fairly brisk increase, marking a new high for the labor force. That means a lot more people started actually looking for work. (Series: Federal Reserve Economic Data (FRED) – CLF16OV, civilian labor force 16 years and over). During that same time period, disability fell by 303,000. Perhaps some of the workforce previously disabled by “COVID” have started to recover. Let’s hope they avoid getting reinfected by “COVID” when the new bi-valent “COVID” is released this month by Pfizer, having tested this “COVID” on eight mice to ensure it is both Safe and Effective. (Source – Igor Chudov)

The pop in payrolls on Friday at 08:30 caused a 4-hour rally in equities, but the rally didn’t last; equities sold off through end of day, ending the week down by 3.29%. That wasn’t a great look. The weekly sector map for equities looked bearish, with tech (-5.29%) and materials (-5.14%) leading the market lower, while utilities (-1.49%) did best. Utilities performing best, tech doing worst = bearish. Standard and Poor’s 500 (SPX) also closed below the 9 MA, which is a short term bearish signal.

Crappy debt (JNK) also plunged, losing 2.14% – you can see that the JNK chart is uglier than that of SPX (although it has a shorter timeframe), and it is quite close to breaking down below the previous low. JNK is also signaling risk off.

The buck moved higher on the week, rising 0.70%, making a new 20-year high. For its part, EUR/USD fell 0.37% to 0.996; that’s not a new low, but the close below 1.00 is still a bad sign. A strong dollar is generally a risk-off signal; another new 20-year high shows a really strong dollar.

Gold fell 27.20 [-1.55%] on the week, some of which was the strong dollar effect. Gold/Euros fell too, but only by 1.19%. You can see that OI (open interest) remains quite low, which hints at a low for gold – but with all the fuss in Europe, currency moves appear to be dominating the price of gold at the moment. Possibility: if/when

by davefairtex

by davefairtex