Executive Summary

- Why purchasing power and quality of life will decline in OECD countries, even as economic 'growth' is maintained

- Why 'energy mix' is as critical as 'energy supply'

- The potential of natural gas as a "bridge" fuel

- Why we're inheriting a "slower moving" world

If you have not yet read Part I: The War Between Credit and Resources, available free to all readers, please click here to read it first.

Low-Quality GDP

Declinists have been surprised by the ability of policy makers to slow the rate of our post-Peak-Oil financial collapse using quantitative easing. But the global economy stopped funding new industrial growth with oil starting seven years ago. Accordingly, the transition to coal as the source to fund growth was well underway before the financial crisis began.

And it remains vexing, to be sure, to understand how the world economy has been able to move forward – at least a little – in the post-2008 environment.

Nevertheless, we now have those answers and no longer need to forecast an imminent black swan or tail event: either collapse or a large upside surprise. Instead, by continuing to piece together constant reflationary policy in combination with natural gas and coal resources, the world's been able to leverage the forward motion of large populations in the Non-OECD countries to produce a hobbled version of economic “growth.” This is not fast growth. And this version of growth is not improving our life quality. Global industrial growth now is now dirtier than ever, as the next layer of fossil fuels begins to be extracted.

The global economy therefore is rebounding but it's doing so even as incomes and purchasing power decline in the OECD.

When recent data was released (again by the Census Bureau) showing that U.S. incomes had continued their decline, this time back to 1996 levels, many analysts wondered how the economy could still be growing as incomes fall. A simple answer is that GDP is composed of a number of economic inputs, and the U.S. can enjoy, for example, strong exports and strong corporate profit growth – plugging into demand in the developing world – while life quality declines for U.S. workers. This low-quality GDP will broadly define economic life over the next decade.

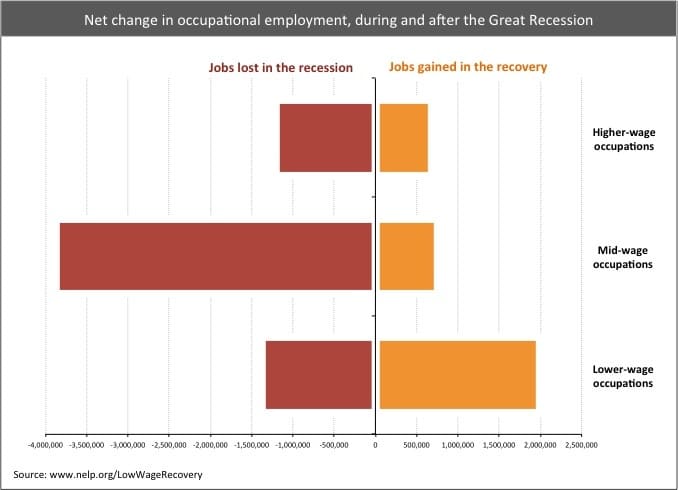

Net Change in Occupational Employment, During and After the Great Recession

(Source – National Employment Law Project)

In the same way

by cmartenson

by cmartenson