Consumer Economy

Personal Income (PI); 25.858T +210.1B (+0.81% m/m),

Auto/Light Truck Sales (ALTSALES); 17.2M -581.0K (-3.37% m/m)

Durable Goods, New Orders (DGORDER); $296B -19.9B (-6.73% m/m)

GDP (GDP); 29.977T +252.8B, (+0.84% q/q)

This month, Durable Goods reversed last month’s big (tariff-driven?) increase. Auto/Light Truck sales also fell, but this month’s decline (about 581k units) was just 31% of last month’s increase of 1.87M – and ALTSALES remains near a 4-year high.

GDP, unadjusted for inflation, rose an annualized 3.4%. With lying-BLS inflation at an (annualized) 2.3% rate (understated by maybe 8%), that suggests GDP is actually contracting. Even GDP adjusted for fake-BLS-inflation contracted slightly, down 0.06 (-0.24% annualized).

Personal Income was strong this month, rising (annualized) 9.84%. Compare this to the average increase, which has been roughly 5%-6%/year during the Biden-Autopen administration.

Credit & Rates

Fed Balance Sheet (WALCL); 6.673T -15.5B (-0.23% w/w)

Total Bank Credit (TOTBKCR); 18.389T +19.1B (+0.10% w/w)

30 Year Mortgage Rate (MORTGAGE30US); 6.89% +3 bp

10 Year Treasury (DGS10); 4.41% -10 bp

20+ Year Bond Fund (TLT); 86.28 +1.73 (+2.05%)

More QT this week, alongside a moderate expansion (5.2% annualized) of bank credit.

Over the last 4 weeks, annualized bank credit has been about 5.4%. That’s not deflationary.

The 10-year yield fell this week, and so the bond fund TLT rallied. The candle print for TLT was a mild bullish reversal, but TLT remains in a weekly downtrend. Ed Dowd is still bullish on TLT due to the contraction he sees coming. I’m still not long.

Risk-off coming. [May 30]

(source – dowdedward)

This week, money flowed into all US treasury instruments, but it especially liked the long bonds, with the 10-12 basis point drop seen in the 10-30 year instruments. It looks like the US treasury collapse may have been put on hold. This feels like “risk off”.

CME Fedwatch Tool projects a 2% chance of one cut at the June 18th meeting. No Cuts For You!

Currencies

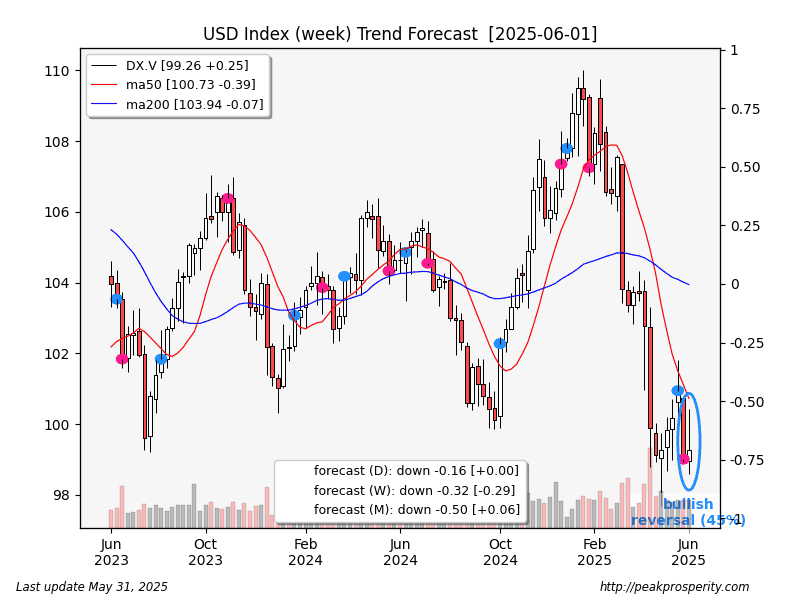

The buck tried to rally this week but mostly failed, moving up just 0.25 (+0.25%) to 99.26. The buck remains in a downtrend. After last week’s almost 2% decline, this was a pretty pathetic bounce.

Losers: GBP [-0.36%], RMB [+0.28%], AUD [-0.73%], JPY [+0.96%]

Metals

Gold fell 50.40 [-1.50%] to 3315.40, which pulled gold into

by thc0655

by thc0655