Consumer Economy

Auto/Light Truck Sales (ALTSALES); 15.3M -260K (-1.69% m/m)

Big picture: This was a small drop, but the trend is not your friend. Declining auto sales is (mildly) recessionary.

Heavy Truck Sales: 3-year low.

Auto Sales: 5-year low.

Overall: 1 year low.

Credit & Rates

Fed Balance Sheet (WALCL); 6.66T +2.3B (+0.03% w/w)

Total Bank Credit (TOTBKCR); 18.53T +47.5B (+0.26% w/w)

30 Year Mortgage Rate (MORTGAGE30US); 6.72% +0.00 (+0.74% w/w)

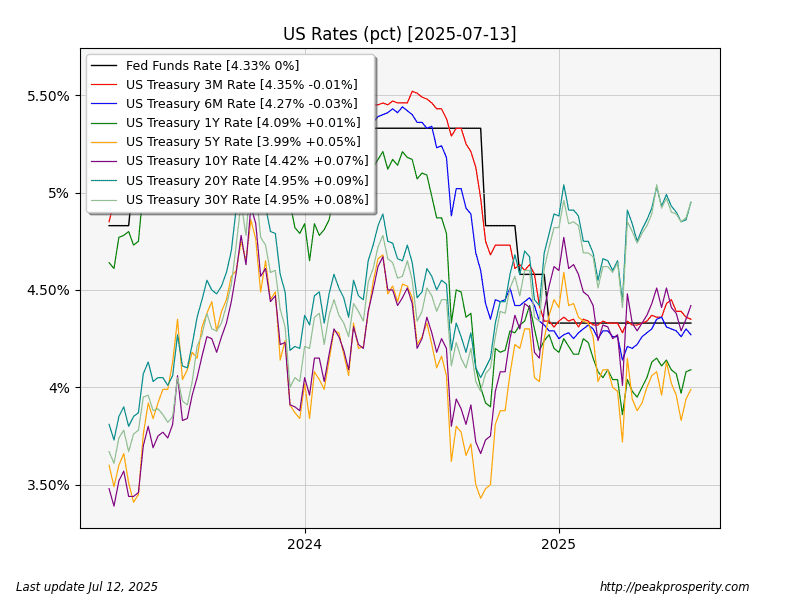

10-Year Treasury (DGS10); 4.42% +7.0

20+ Year Treasury ETF (TLT); 85.79 -1.18 (-1.36%)

No QT.

Big expansion of bank credit: 13.5% annualized. Inflationary.

Money left the long end of the curve; 10-30 year items rose 7-9 bp this week (which means TLT loses 1.36%), but moved slightly into the short end (with 3 and 6 month rates falling by 1-3 bp). With FedFunds at 4.33%, the 6M at 4.27%, and the 1-year at 4.09%, it feels as though the Treasury market is projecting “problems ahead” for at least a year (4.09%) – but nothing serious in the next 3 months (4.35%).

This time projection from interest rates lines up with my “recession, but only at the right time” prediction from last week.

CME Fedwatch Tool projects a 5% chance of one cut at the July 30th meeting, in spite of the rumors about Powell.

Fed Chair Jerome Powell reportedly considers resigning, William Pulte hints [July 11]

(source – yahoo)

Currencies

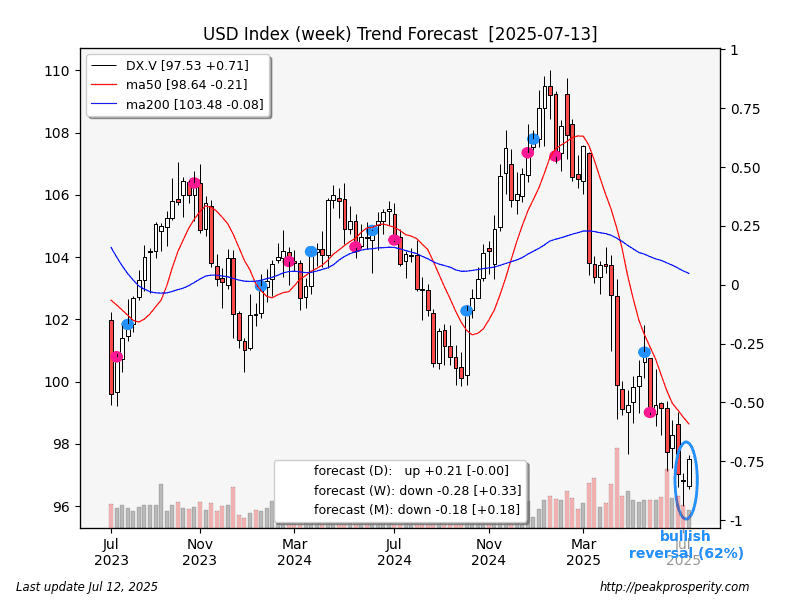

The buck deconfettied reasonably strongly, rising 0.71 [+0.73%], with the daily now back in an uptrend. The “swing low” candle print looked quite bullish. Is the downtrend for the buck over?

Losers: EUR [-0.75%], GBP [-1.07%], JPY [+2.00%], CAD [+0.61%]

Winners: mining-country AUD [+0.35%]

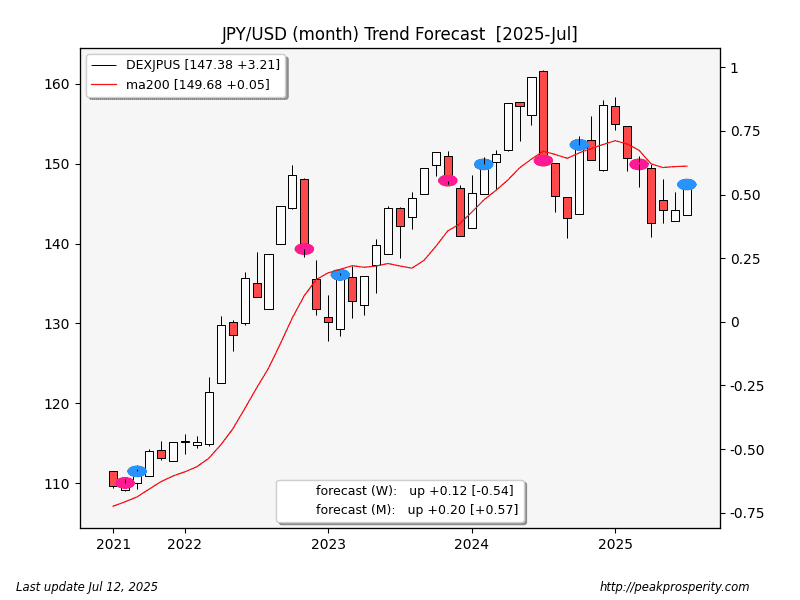

We’re not at a catastrophe point yet for Japan, but the trend doesn’t look great. Here’s the “monthly JPY” trend model, which appears to have been pretty accurate over time. Higher JPY/USD = bad if you live in Japan.

China cutting off rare earth minerals – not expensive to mine, but manufacturing doesn’t work without these elements – may be causing “some difficulty” for Japan.

Japan’s rare-earth imports from China plunge to 5-year low [July 10]

72% drop in value for May follows trade curbs by Beijing

(source – nikkei)

The 10-year JGB yield looks “unpleasant” – it may be ready to break out to new highs. That’s really bad if you own the

by cmartenson

by cmartenson