Consumer Economy

- Auto/Light Truck Sales (ALTSALES) 16.3M +606.0K (+3.85% m/m) (prior +6.18% m/m)

- Durable Goods, New Orders (DGORDER) 318.9B +2.6B (+0.83% m/m) (prior -1.16% m/m)

- GDP (GDPC1) 24.17T +118B (+0.49% q/q)

- Personal Income (PI) 26.84T +149.2B (+0.56% m/m) (prior +0.00% m/m) +278.8B [+1.05%] y/y

Auto/light truck sales bounced back to neutral – mostly that’s about light trucks, since Americans don’t like autos any longer (auto sales fell to a new post-COVID low). Heavy truck sales (my recession indicator) moved lower, but did not make a new multi-year low. Call it mildly recessionary.

Durable goods moved higher – it wasn’t a new high, but orders remain near the top of the range, so that’s not recessionary.

Personal Income rose 0.56% this month; that’s definitely not keeping up with Bibi-flation. GDP [allegedly adjusted for inflation] was up about 2% annualized. Not BOOMING.

Credit & Rates

- Total Bank Credit (TOTBKCR) 19.46T -16.1B (-0.08% w/w)

- Fed Balance Sheet (WALCL) 6.70T -7.5B (-0.11% w/w)

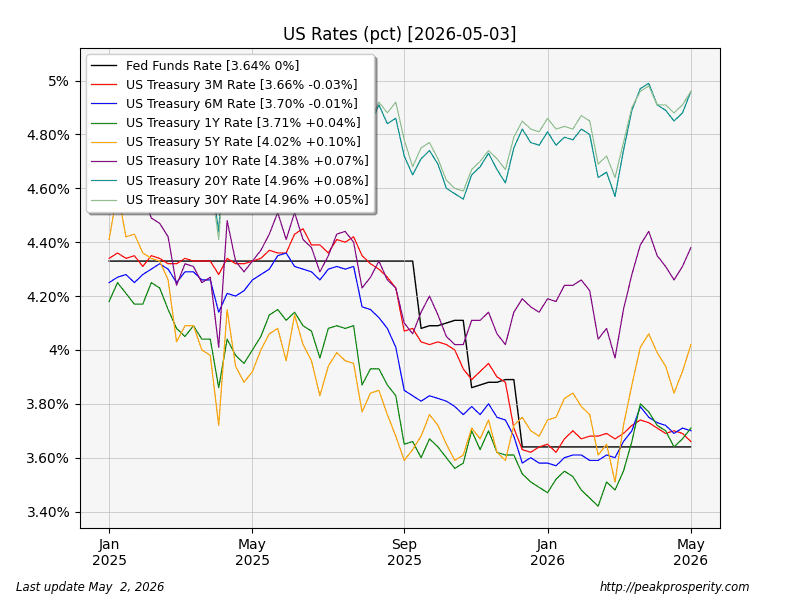

- US 30 Year Mortgage Rate (MORTGAGE30US) 6.30% +7 bp

- 3-Month Treasury (DGS3MO) 3.66% -3 bp

- 1-Year Treasury (DGS1) 3.71% +4 bp

- 5-Year Treasury (DGS5) 4.02% +10 bp

- 10-Year Treasury (DGS10) 4.38% +7 bp

- 20+ Treasury ETF (TLT.N) -1.27% w/w

There was a contraction in bank credit this week. While the weekly series often bounces around, if it continues to move lower, that’s recessionary.

The Fed also reverse-printed money this week; $7.5 BILLION was un-printed. That happens sometimes, too.

The 3-month Treasury had another week of inflows [yields dropped], while money fled the middle of the curve [yields rose] – especially the 5-year, which saw a 10 bp increase. TLT had a bad week, too. My guess: money is going into the 3-month for safety (“recession”), but fleeing the medium-term due to concerns about the prospect for a (5-10 year) Bibi-flation period. You can see the moves in the index below, with the 5Y rate (yellow line) rising the most.

The Fed meeting produced no rate cut – and no rate increase. This week was Powell’s last press conference as Chairman – Trump is replacing him with Warsh.

Regime Change: Powell, Chair of Mega-QE & “Ample Reserves Regime,” to Be Replaced by Warsh, who Wants a Smaller Balance Sheet [May 1]

(source – wolfstreet)

- Powell will remain on the board until

by davefairtex

by davefairtex