Consumer Economy

Retail Sales (RSAFS) $732B +4.6B (+0.63% m/m)

Industrial Production (INDPRO) 103.9 +0.10 (+0.10% m/m)

US Housing Permits (PERMIT) 1.31m -50k (-3.67% m/m)

US Housing Starts (HOUST) 1.30m -122k (-8.54% m/m)

Retail Sales grew at an annualized rate of 7.56% – that’s decent expansion, and not recessionary. The Food & Bev segment grew just +0.28% m/m, but clothing +1.01% m/m, and “non-store” sales (online) +1.98% m/m. A Bezos win.

Industrial Production isn’t climbing, but remains close to the all-time high [104.21] set in June 2025.

Both Housing Permits and Housing Starts fell – it was a new 5-year low for permits, and it is nearing a breakdown for starts too. Permits are the leading indicator. First, you get a “permit”, and then you can “start” building. Related: some places make it really hard to get a permit – LA after that land-clearing “wild” fire on January 7th, 2025. LA County has a dashboard: 12,048 destroyed parcels, 1,943 rebuild applications, with just 393 permits issued. Who benefits? I digress.

Credit & Rates

Fed Balance Sheet (WALCL) $6.61T +2.6B (+0.04% w/w) (prior +0.06% w/w)

Total Bank Credit (TOTBKCR) 18.72T +28.8B (+0.15% w/w) (prior -0.21% w/w) +751.5B [+4.02%] y/y

30 Year Mortgage Rate (MORTGAGE30US) 6.26% -0.00 (-1.44% w/w) (prior -2.36% w/w) -0.01 [-9.42%] y/y

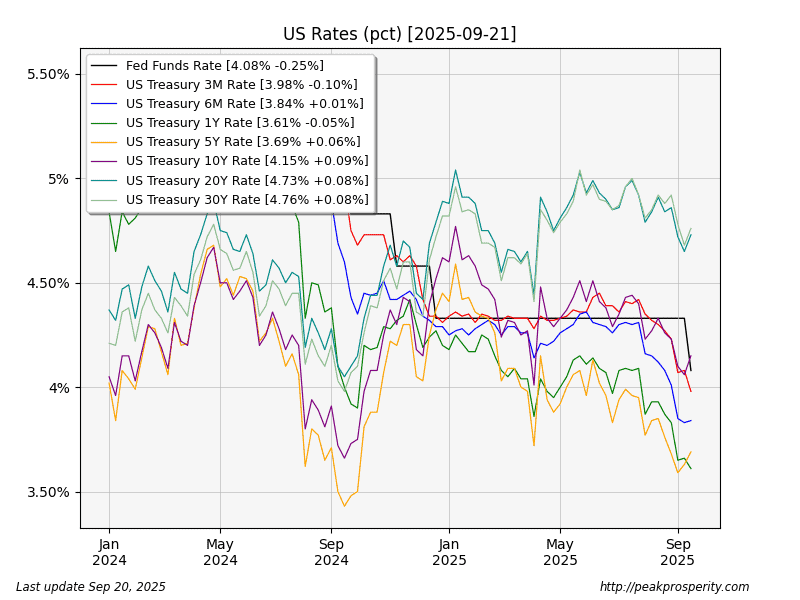

3-Month Treasury (DGS3MO) 3.98% -10 bp

10 Year Treasury (DGS10) 4.15% +9 bp

30 Year Treasury (DGS30) 4.76% +8 bp

20+ Year ETF (TLT) 89.02 -0.93 (-1.03% w/w)

No QT this week.

Bank credit remains choppy; last week saw a drop [-39B], while this week bounced back, but it was not a new high. Overall, bank credit is not expansionary.

This week, money moved into the 3-month and 1-year (i.e., yield fell), and moved out of the longer end of the curve (yields rose). This suggests a prediction of short-term (deflationary) pain, alongside longer-term inflationary … pain. The Fed Funds rate is still higher than everything up to the 5-year treasury; the market is already cutting short-term rates more than the Fed has done.

As a result of the selling in longer-dated bonds, TLT saw a loss. It rallied briefly post-Fed-announcement, but then sold off for the remainder of the week. Most of the losses came before market open on

by westcoastjan

by westcoastjan