Consumer Economy

Durable Goods, New Orders (DGORDER); DELAYED

Nonfarm Payrolls (PAYEMS); DELAYED

ISM Manufacturing Index; 49.1 (< 50 is contraction)

Consumer Confidence (conference-board); 94.2 (< 100 is contraction)

The two series we have values for are hinting at contraction.

Payrolls and orders are delayed this week due to the “Government Shutdown.”

Elizabeth Warren calls for Trump to release the jobs report despite shutdown [Oct 3]

(source – yahoo)

Given Warren’s enthusiasm, and given that Trump isn’t demanding release, I’m guessing it is bad news.

Credit & Rates

Fed Balance Sheet (WALCL) 6.59T -21.3B (-0.32% w/w) (prior -0.00% w/w)

Total Bank Credit (TOTBKCR) 18.73T +21.8B (+0.12% w/w) (prior +0.01% w/w) +761.4B [+4.06%] y/y

30 Year Mortgage Rate (MORTGAGE30US) 6.34% +4 bp

3 Month Treasury (DGS3MO) 3.95% -7 bp

10 Year Treasury (DGS10) 4.12% -8 bp

30 Year Treasury (DGS30) 4.71% -6 bp

20 Year Bond Fund (TLT) 89.38 +0.54%

We saw some QT this week (negative money printing!), and bank credit actually expanded (+6.24% annualized).

Rates moved lower; money flowed into both short, medium, and long-dated bonds. That caused TLT to move higher, but it was a modest move. The 3-month Treasury (-7 bp this week), which Ed Dowd likes to follow, appears to be leading Fed Funds lower. The 3-month period does the “cut” (or the “raise”), and then the Fed follows.

CME Fedwatch Tool projects a 96% chance of one cut on the October 29th meeting.

Currencies

The buck confettied a bit this week, losing 0.41 [-0.42%] to 97.42. Most of the damage happened on Monday/Tuesday. The buck remains in a slight weekly/monthly uptrend. So far, no confirmation from the buck regarding the upcoming War in Europe.

Winners: EUR [+0.41%], GBP [+0.54%], JPY [-1.36%], AUD [+0.98%]

Metals

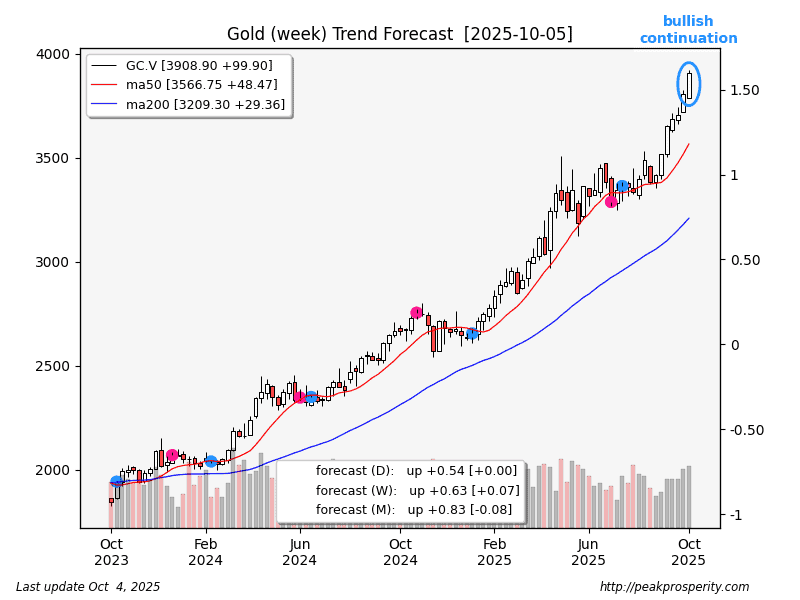

Glorious Gold rose 99.90 [+2.62%] to 3908.90, which is a new all-time high. Most of the gains came on Monday and Friday. Gold suffered a pair of smashes (Tuesday: -$80, Thursday: -$78); the smashes happened during European (Tuesday) and US (Thursday) trading hours. The Thursday smash happened right after gold made a new all-time intraday high to $3923.30.

In spite of the smashes, gold ended the week in an uptrend in all 3 timeframes.

Gold open interest actually declined this week [-9.1k]; that’s probably because of the 30k contracts that stood for delivery. That’s

by jim-h-2

by jim-h-2