Consumer Economy

Consumer Sentiment (UMCSENT); 55.0

Consumer Credit (TOTALSL); 5.03T +363M (+0.01% m/m)

Consumer sentiment looks pretty unhappy – it is about as bad as it was back in 2008. It was even lower under Senile Joe-Autopen, during the recession that was hidden by “them” giving illegals trillions of our tax dollars. “We’ll pay for your hotel. Yes, really.”

Consumer credit (pct change y/y) is about flat, which says no growth in credit, even though inflation remains high. Credit growth is as low as it was during the Fauci-lockdowns back in 2020. Consumers are tapped out, or have no confidence – maybe both. That’s recessionary.

Credit & Rates

Fed Balance Sheet (WALCL) 6.59T +3.7B (+0.06% w/w)

Total Bank Credit (TOTBKCR) 18.76T +20.1B (+0.11% w/w)

30 Year Mortgage Rate (MORTGAGE30US) 6.30% -0.00 (-0.63% w/w)

3 Month Treasury (DGS3MO) 3.95% -8 bp

10 Year Treasury (DGS10) 4.04% -9 bp

20 Year Treasury (DGS20) 4.58% -11 bp

20 Year Bond Fund (TLT) 90.62 +1.24 (+1.39% w/w)

No QT, and total bank credit expanded slightly again, at 5.72% annualized. That’s “just barely expansion”, but we are out of deflationary mode. Note that consumers apparently didn’t contribute to this credit increase.

Bond rates moved lower, with maybe 40% of the decline happening on Tariff Terror Friday. TLT was a big winner on Friday: +1.61%.

Nudge Google seemed excited – about Tariff Terror, as well as the Schumer Shutdown.

Trump announces 130% tariffs on China. The global trade war just came roaring back [Oct 10]

(source – CNN)

Whew! Trump Crash (because “tariffs”) is back on the schedule! Curiously, people want to buy U.S. Treasurys in response. TLT is now in an uptrend.

CME Fedwatch Tool projects a 98% chance of one cut on the October 29th meeting.

Currencies

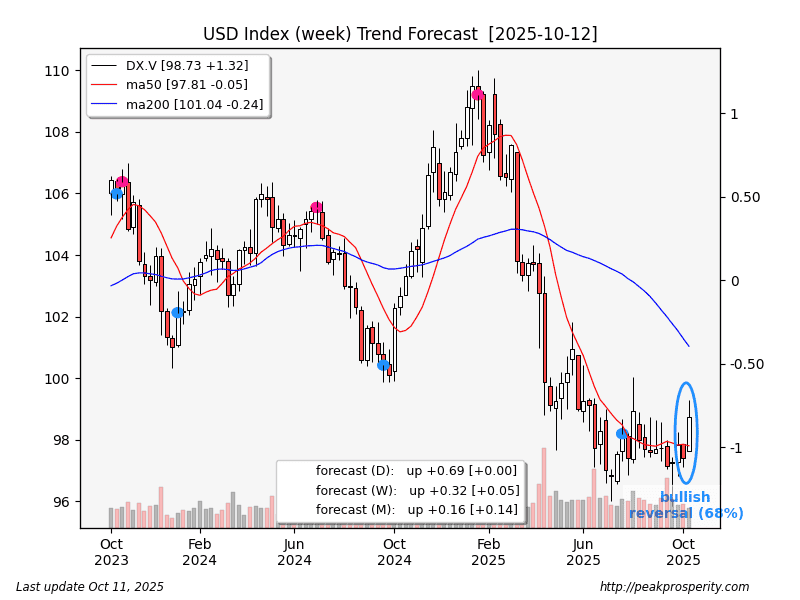

The buck rallied strongly this week, rising 1.32 [+1.35%] to 98.73 – and that’s including Friday’s plunge (-0.55 -0.56%) caused by the Tariff Terror news. The buck is now in a moderately strong uptrend in all 3 timeframes. That really does look like a bullish reversal to me.

Losers: Euro [-1.14%], GBP [-0.96%], JPY [+3.24%], AUD [-1.90%], CAD [+0.39%].

The Euro appears to be on the edge of a bearish reversal. I mean, it looks like it’s had one

by cmartenson

by cmartenson