Consumer Economy

- Producer Prices (PPIACO) 261.5 +0.71 (+0.27% m/m)

- Consumer Sentiment (UMCSENT) 56.40 +3.50 (+6.62% m/m)

Producer prices ticked higher – 3.2% annualized. That’s not particularly inflationary.

UMCSENT (U-Michigan consumer sentiment survey) continued to rise off the near-all-time lows; its an ugly chart (which looks horrifically recessionary), but it is now showing minor improvement.

That said, the survey was revealed to have a “significant bias.” What is the bias? Coincidentally, the survey shifted in 2024/2025 to target “mostly donkeys” – now at 64% of those surveyed (vs 36% elephants) – from being relatively even in the years prior. It turns out, Donkeys are really bearish about the economy (because Trump = Hitler?), and they’ve pulled the sentiment index down to historically low levels. Zero Hedge has the charts – right at the end of the article. Maybe it’s a 20-point bias?

Inflation Fears Plummet As UMich’s Democratic Bias Is Exposed [Feb 20]

(source – zerohedge)

Credit & Rates

- Total Bank Credit (TOTBKCR) 19.26T +19.5B (+0.10% w/w)

- Fed Balance Sheet (WALCL) 6.61T +402.00M (+0.01% w/w)

- US 30 Year Mortgage Rate (MORTGAGE30US) 5.98% -3 bp

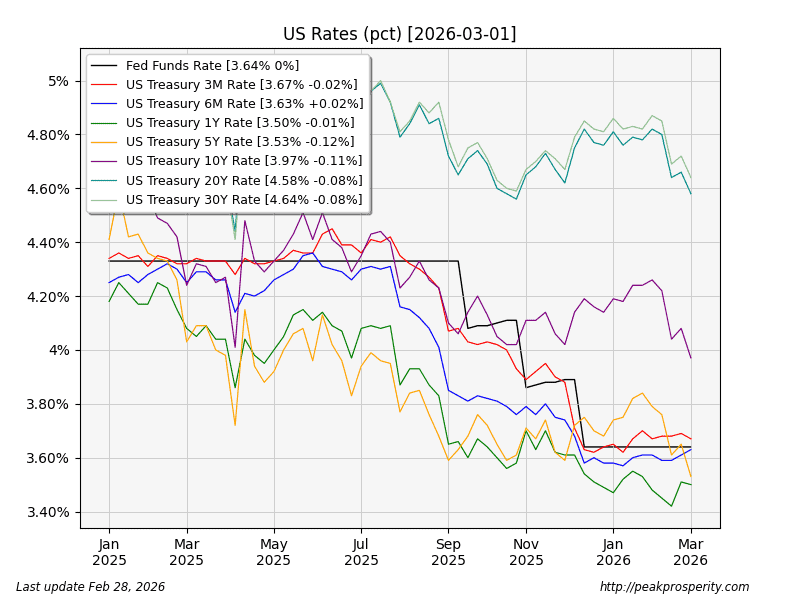

- 3-Month Treasury (DGS3MO) 3.67% -2 bp

- 1-Year Treasury (DGS1) 3.50% -1 bp

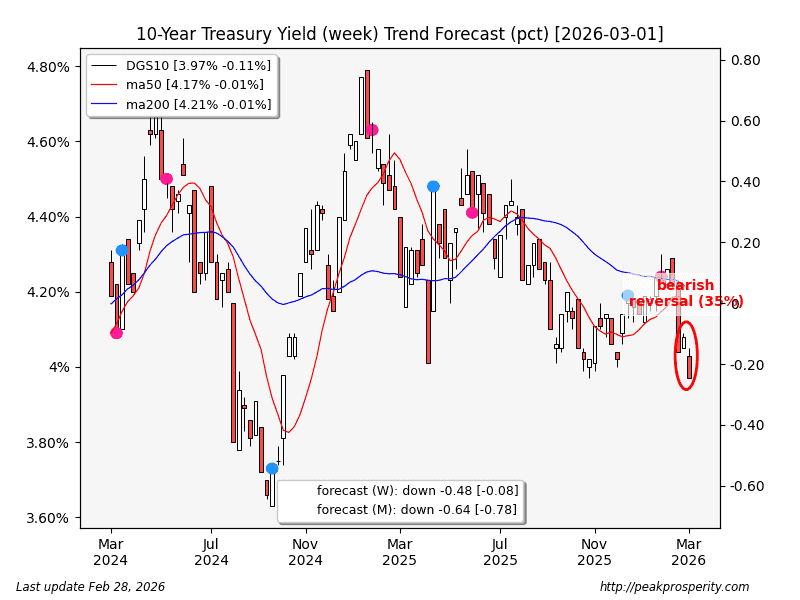

- 10-Year Treasury (DGS10) 3.97% -11 bp

- 20+ Treasury ETF (TLT.N) +1.58% w/w

- AAA-10Year (AAA10Y) 1.20% +2 bp

Bank credit was just barely expansionary (5.2% annualized), and the Fed didn’t do any “money printing” this week at all, in spite of all those “private credit” signals we saw last week.

Confidence in US treasury bonds (vs corporates) remains intact – it even increased a bit this week (+2 bp) to 1.20%.

The short end of the curve was mostly unchanged [suggesting no rate cut ahead], but the big news was in long rates: money gushed into the long end of the curve, with the 5-30 year bonds dropping 8-12 basis points. TLT had a nice rally as a result, rising 1.58%. That’s a nice move for one week, considering the 20-year provides you 4.58% per YEAR.

You can see the falling 10-year yield below; the last time the 10-year was at 3.97% was back in 2024. Of the 11 bp decline, 5 bp happened on Friday. DGS10 is in a weekly/monthly downtrend. This is a clear risk off signal.

CME Fedwatch Tool projects

by thc0655

by thc0655