Consumer Economy

Industrial Production (INDPRO) DELAYED

Producer Price Index (PPIACO) DELAYED

Housing Starts (HOUST) DELAYED

Retail Sales (RSAFS) DELAYED

Is the Schumer Shutdown a Trump-cession cover-up? At first glance, the Donkeys seem to be idiots to hide this (likely) event. Unless, perhaps, their “strategists” ($20 million spent to figure out why young men hate them) felt that the timing of the arrival of Trump-cession needs to be closer to the midterms than I realized. And/or, perhaps their sources inside government are suggesting the recession data isn’t yet compelling enough to release. I’m pretty sure there’s a scam going on – I’m just not sure what the specifics happen to be. They still don’t invite me to the meetings.

Credit & Rates

Fed Balance Sheet (WALCL) 6.60T +5.6B (+0.09% w/w)

Total Bank Credit (TOTBKCR) 18.76T +1.1B (+0.01% w/w) (2.6% annualized)

30 Year Mortgage Rate (MORTGAGE30US) 6.27% -3 bp

3 Month Treasury (DGS3MO) 3.94% -8 bp

10 Year Treasury (DGS10) 4.01% -4 bp

20 Year Treasury (DGS20) 4.57% -3 bp

20+ Year Fund (TLT) 91.20 +0.58 (+0.64% w/w)

Money moved (gently) into bonds this week, in spite of the bounce in risk assets. TLT’s rally (a new 6-month high) aligned with the drop in the 10-year yield to a new 1-year low. The last time we saw DGS10 at 4.01% was back in October 2024. Most of the bond rates are below the Fed Funds, which is currently 4.11%. The market is (as usual) cutting rates in advance of the Fed – just what you’d expect if the economy was BOOMING. (That’s a joke, son.)

The downtrend in DGS10 – breaking below the prior low – is a positive outcome if you own TLT – I have a position.

CME Fedwatch Tool projects a 100% chance of one cut at the Oct 29th meeting.

Currencies

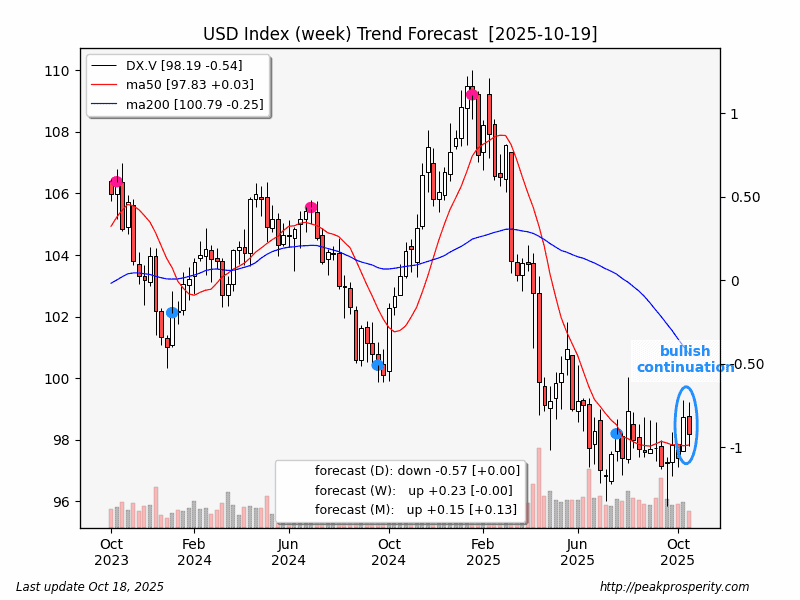

The buck fell 0.54 [-0.55%] to 98.19. The losses came Tuesday-Thursday, with a slight rebound on Friday [+0.10%]. This week’s decline was enough to pull the buck into a daily downtrend. Hopefully, this is just a blip in the dollar recovery.

Winners: EUR [+0.56%], GBP [+0.62%], JPY [-0.99%], CAD [+0.27%]

Metals

On the week, Glorious Gold screamed higher, rising 212.90 [+5.32%] to 4213.30. On Friday, gold

by jhgoodwin

by jhgoodwin