Consumer Economy

Durable Goods (DGORDER) DELAYED

Gross Domestic Product (GDP) DELAYED

Personal Income (PINCOME) DELAYED

Credit & Rates

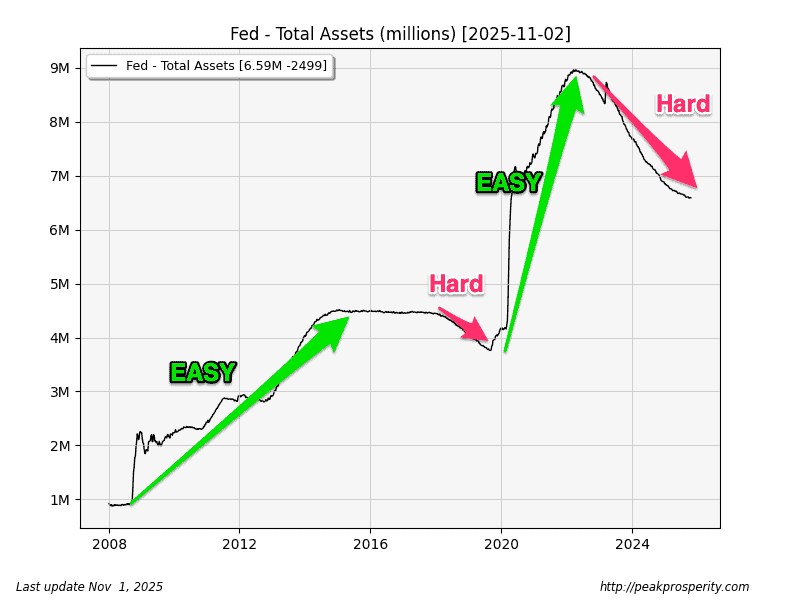

Fed Balance Sheet (WALCL) 6.59T -2.5B (-0.04% w/w)

Total Bank Credit (TOTBKCR) 18.83T +24.3B (+0.13% w/w)

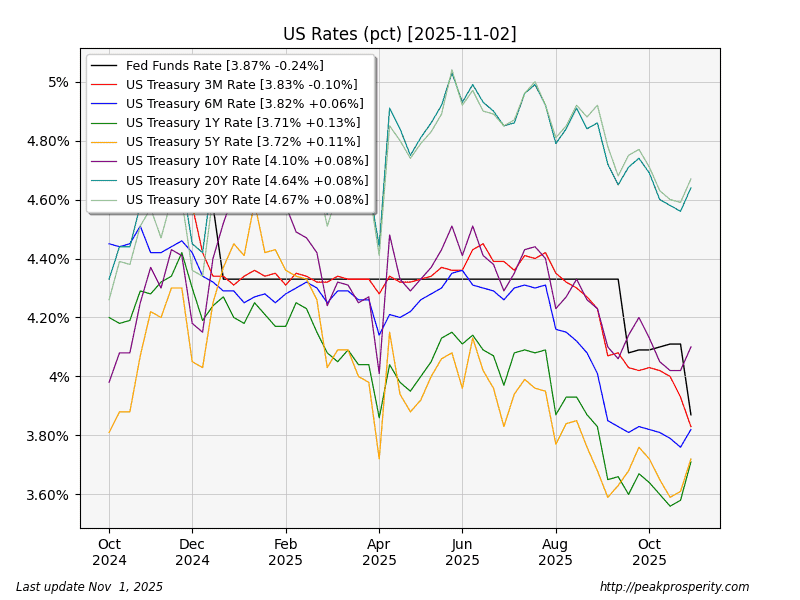

30 Year Mortgage Rate (MORTGAGE30US) 6.17% -2 bp

Fed Funds (b) 3.87% -25 bp

3 Month Treasury (DGS3MO) 3.83% -10 bp

1 Year Treasury (DGS1) 3.71% +13 bp

10 Year Treasury (DGS10) 4.10% +8 bp

30 Year Treasury (DGS30) 4.67% +8 bp

The Fed declared that QT is now over; you can see from the chart that QE = EASY, while QT = HARD. In terms of scale, the 1.3 trillion (produced by “magic money machines”?) hiding in the Cayman Islands comprises about 25% of all the money printed by the Fed since the Safe & Effective (Event 201) printing operation started back in late 2019.

Mostly as a result of the Fed announcement on Wednesday, money moved into the short-duration 3-month items (red), and out of literally everything else. If you look at the math, the market is pricing in “No More Cuts For You” – and longer term, it sees higher rates ahead. The most exciting move: a 13 bp increase in the 1-year. That provides (perhaps) a time horizon too.

Near term: no cuts. Longer term: inflation. TLT was not pleased at this outcome [-1.29%].

The CME Fedwatch Tool appears to be a lagging indicator; it predicts a 63% chance of one cut on the Dec 10th meeting, while the 3-month treasury (red line) is currently predicting no cuts at all.

Currencies

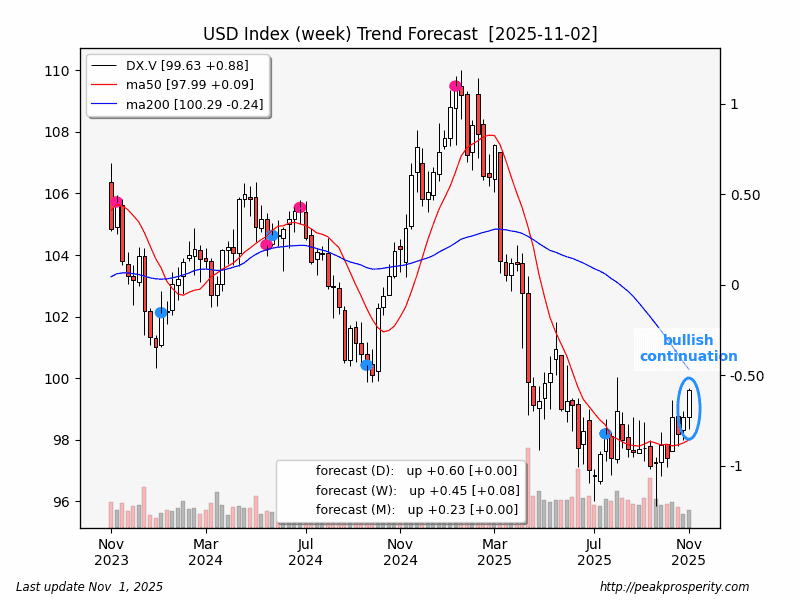

The buck de-confettied strongly this week, rising 0.88 [+0.89%] to 99.63. This marked a new 6-month weekly closing high. The dollar rally started right after Powell said (during the Fed press conference on Wednesday, around 14:35-14:40) that another rate cut is not a sure thing. The dollar rally lasted through the afternoon on Friday.

Losers: EUR [-0.78%], GBP [-1.22%$], JPY [+0.85%]

Winners: AUD [+0.48%]

Immediately after Powell said this on Wednesday, the JPY and the Euro started to turn into confetti. Wolf explains why, although he doesn’t use that term.

The US Dollar Gets More Fuel from Powell’s Doubts about December Rate Cut [Oct 30]

The Fed’s policy interest rates, at 3.75% to 4.0%, are among the highest of the developed economies. They’re

by wotthecurtains

by wotthecurtains