Consumer Economy

Industrial Production (INDPRO) 101.8 +0.18 (+0.17% m/m)

Auto/Light Truck Sales (ALTSALES) 15.6M +299.0K (+1.96% m/m)

Durable Goods, New Orders (DGORDER) 307B -6.8B (-2.17% m/m)

GDP (GDP) 31.10T +609.4B (+2.00% q/q) [+4.26%] y/y

Industrial Production: initially higher through July 2025, now mostly flat.

Auto/Light Trucks Sales: a bounce (+24% annualized) after a longish decline.

Durable Goods: peaked in May 2025, slightly higher y/y.

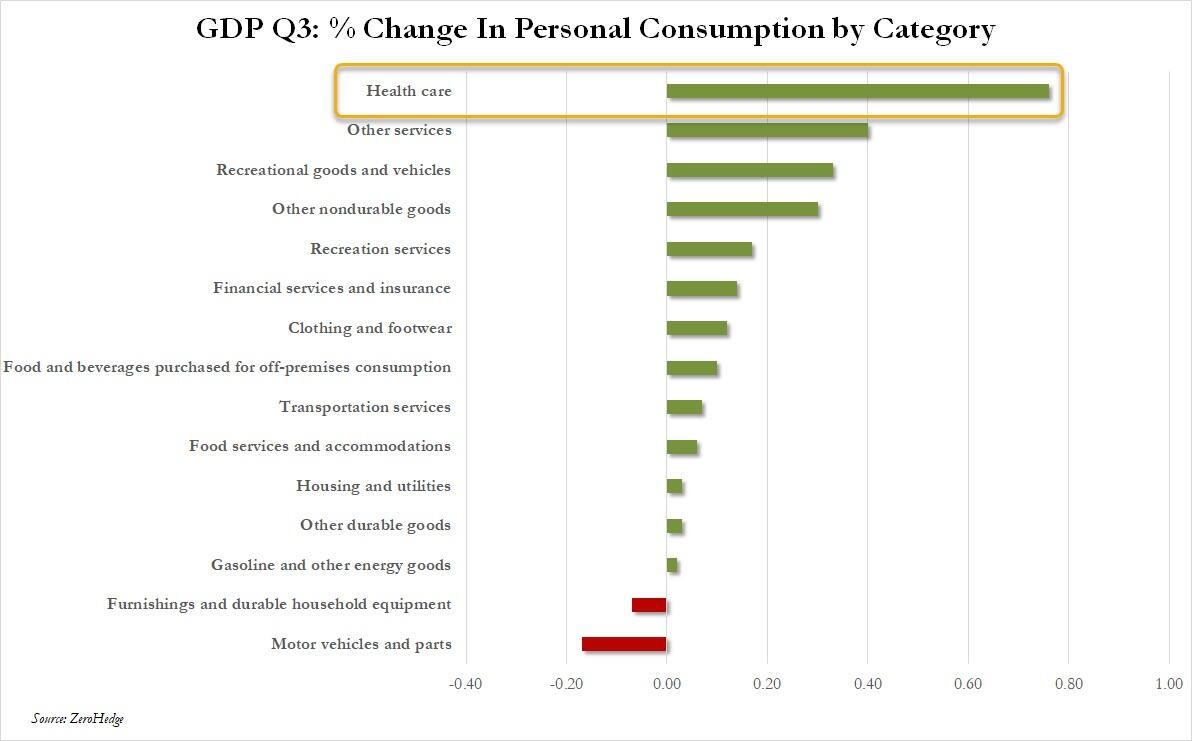

GDP: BOOMING!!! (*)

While the overall auto/light-trucks was “just ok”, Heavy Truck Sales look sickly; there was a YUGE drop that started in June 2025, and the decline is continuing. The “HTRUCKSSA” series – which has a habit of plunging ahead of recessions – is definitely recessionary.

And about that BOOMING GDP (*). There was a massive increase in consumer spending in one sector:

Q3 GDP Unexpectedly Surges To 2 Year High On Soaring Health Insurance Spending [Dec 23]

(source – zerohedge)

Coincidentally, we have seen an increase of +6.64 million (total population 16+) “With a Disability” ever since “Biden” mandated the shot back in 2021. This was Safe & Effective – for sickcare system income. “Mistakes Were Not Made.”

Credit & Rates

Fed Total Assets (WALCL) 6.56T +17.6B +0.27%

30 Year Mortgage Rate (MORTGAGE30US) 6.18% -3 bp

3-Month Treasury (DGS3MO) 3.64% +2 bp

1-Year Treasury (DGS1) 3.50% -1 bp

10-Year Treasury (DGS10) 4.15% -1 bp

30-Year Treasury (DGS30) 4.83% +1 bp

20+ Year ETF (TLT) 87.74 +0.19 +0.22%

Money printing (“ample reserves”) this week by the Fed – around $18 billion. Last week looked boring; this week’s (annualized) increase was 14%, which will be a trend change, if it continues.

No data for bank credit this week.

Not much change in rates this week; the 3-month is suggesting “no rate cut”, while the 1-year thinks we might have another cut eventually = perhaps more than a 50% chance, but it remains sometime in the future.

CME Fedwatch Tool projects a 17.7% chance of one cut on the January 28th meeting.

Currencies

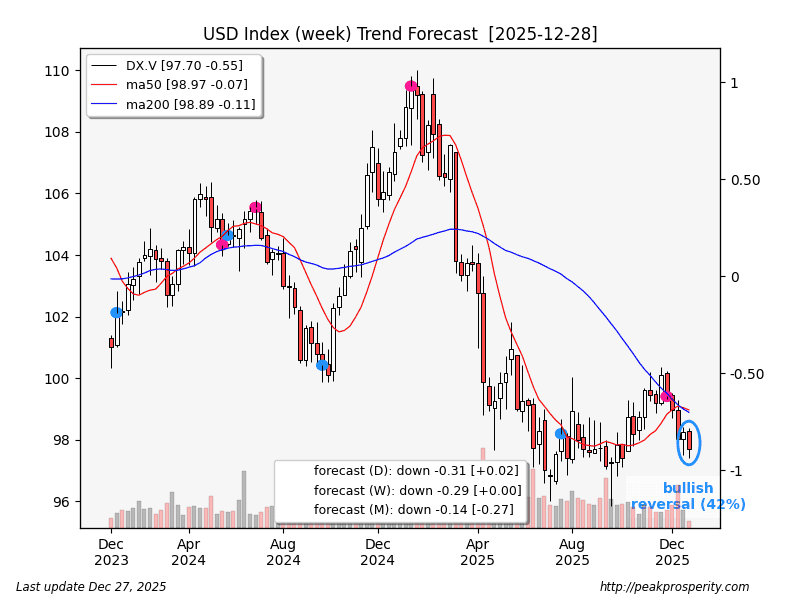

The dollar turned to confetti this week, dropping 0.55 [-0.56%] to 97.70. Losses came on Tuesday/Wednesday. The buck remains in a moderate downtrend in all 3 timeframes.

Winners: EUR [+0.39%], GBP [+0.82%], JPY [-0.54%], AUD [+1.43%], RMB [-0.49%], CAD [-0.81%].

The RMB/USD has done very well over the past 8 months, plunging

by cmartenson

by cmartenson