Consumer Economy

- Personal Income (PI) 26.51T +86.2B (+0.33% m/m)

- GDP (GDP) 31.49T +392.0B (+1.26% q/q)

- Durable Goods, New Orders (DGORDER) 319.6B -4.6B (-1.43% m/m)

- Median New Home Sales Price (MSPNHSUS) 414.4K +16.8K (+4.23% m/m)

- Auto/Light Truck Sales (ALTSALES) 14.8M -1.20M (-7.49% m/m)

- Industrial Production (INDPRO) 102.3 +0.71 (+0.70% m/m)

Personal Income: up 4% (annualized), which is not keeping up with actual inflation.

GDP (unadjusted for inflation) was up 5% (annualized); adjusted for inflation, the rate was just 1.4% (0.35% q/q). There’s a long piece at ZeroHedge about the GDP release. Apparently, the Schumer Shutdown was a big factor.

Of the above, the most notable variable was government spending, which due to the government shutdown in Q4 tumbled by 5.1% – the biggest drop since covid – and subtracted 0.9% from the final GDP number.

Median New Home Sales prices bounced higher, but the trend overall remains down.

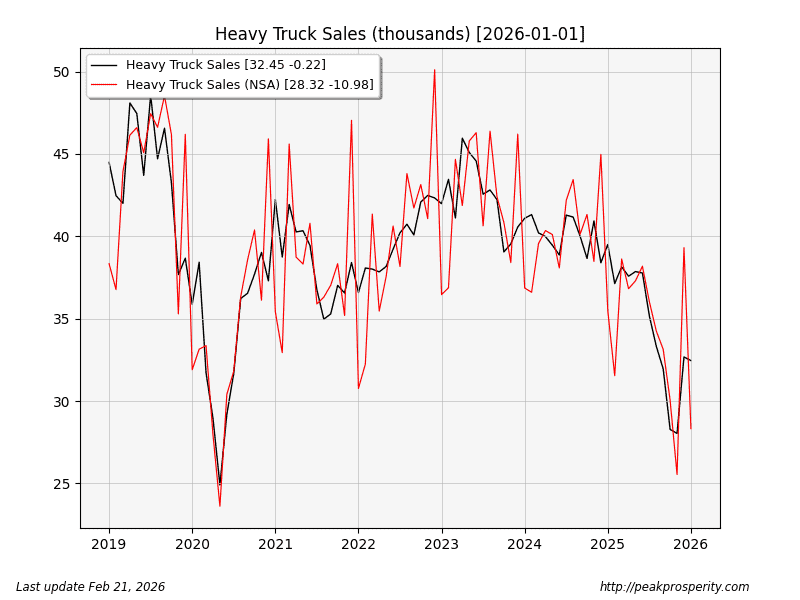

Auto/light truck sales fell to a new 3-year low, and heavy truck sales (not seasonally adjusted) fell back down to pandemic lows. Fun fact I didn’t know: it turns out that companies tend to buy lots of heavy trucks in November. The red line (not seasonally adjusted) vs the black line (adjusted) shows this dynamic. There’s always an HTRUCK spike in November. Regardless of “BOOMING” AI, the heavy truck sales don’t look very good.

Industrial production actually did well – it rose to a 1 year high. Durable Goods (new orders) ticked lower, but it remains in a reasonably strong uptrend. DGORDER gives us a look at next month’s industrial production. Maybe that’s partly why the Industrial/DJI ratio is looking so strong right now.

Credit & Rates

- Total Bank Credit (TOTBKCR) 19.24T +69.6B (+0.36% w/w)

- Fed Balance Sheet (WALCL) 6.61T -9.0B (-0.14% w/w)

- US 30 Year Mortgage Rate (MORTGAGE30US) 6.01% -8 bp

- 3-Month Treasury (DGS3MO) 3.69% +1 bp

- 1-Year Treasury (DGS1) 3.51% +9 bp

- 10-Year Treasury (DGS10) 4.09% +5 bp

- 20+ Treasury ETF (TLT.N) -0.35% w/w

This week saw a crazy expansion of bank credit (19% annualized). I’m going to assume that’s AI doing its bubbling. Meanwhile, the Fed reverse-money-printed a tiny amount this week (if you squint, you can see the slight downtick) – these things tend to

by pdeb

by pdeb