Consumer Economy

Retail Sales (RSAFS) $0.72T +4.6B (+0.63% m/m)

Industrial Production (INDPRO) 104.0 +0.35 (+0.33% m/m)

Producer Prices (PPIACO); 260.2 +1.68 (+0.65% m/m)

Retail Sales (a dollar amount) rose 7.56% annualized – a nice move, maybe even keeping up with inflation, but not a new all-time high due to the big contraction (-6.2B) that happened back in May.

Industrial Production (an index) rose 3.96% annualized – an ok move, but not an all-time high, since INDPRO was slightly higher back during Trump 1.0 (2018).

The PPI rose 7.8% annualized – this is my “producer inflation” metric, and it is driven substantially by energy prices. This version of PPI dates back to 1913.

In combination, no impending recession this month, plus moderate producer inflation.

Credit & Rates

Total Bank Credit (TOTBKCR); 18.54T +12.2B (+0.07% w/w)

Fed Balance Sheet (WALCL); 6.66T -2.6B (-0.04% w/w)

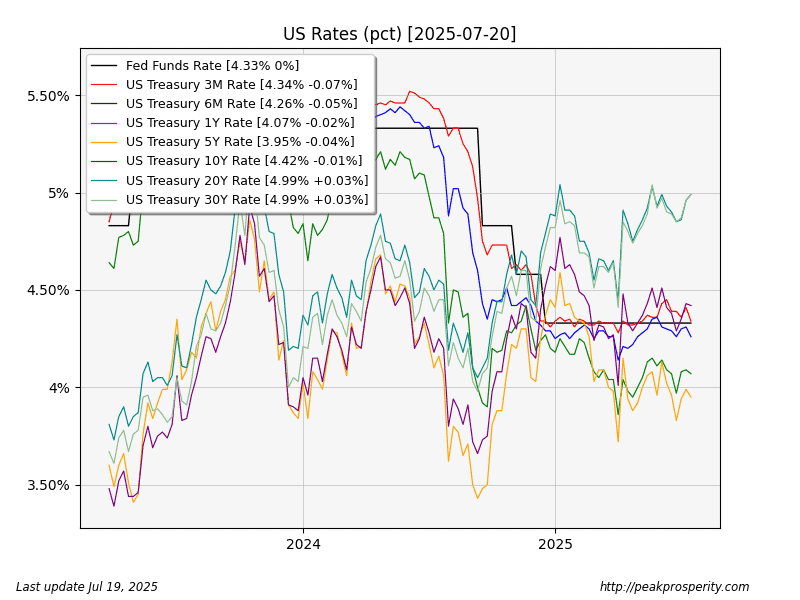

30-Year Mortgage Rate (MORTGAGE30US); 6.75% (+3 bp)

10-Year Treasury (DGS10); 4.42% (-1 bp)

Bank credit grew by 3.6% annualized – that’s deflationary, as it “needs to be” above 5%. Over the last 4 weeks, bank credit has increased (annualized) at 6%. We also had very mild QT (2% annualized).

Regarding rates, money left 20-30 year items (+3bp), and moved into 3M treasurys (-7bp). The 3-month is now (mostly) back to the Fed Funds Rate. If it drops below Fed Funds, that would be a rate cut.

CME Fedwatch Tool projects a 4% chance of one cut at the July 30th meeting.

Probably no Fed rate cut in two weeks. But:

September: 53% chance

October: 75% chance

And the wildcard: Trump says he won’t fire Powell “unless there’s fraud.”

Fed Chair Jerome Powell Responds to Trump’s Fraud Allegations [July 17]

[Trump] dispelled that this week, admitting that Powell isn’t going anywhere unless there’s fraud, a reference to the $2.5 billion renovation project of the Federal Reserve building.

(source – townhall)

So that’s confirmation of sorts – we could have a September/October Trump Crash coming up. Trump knows, and Powell knows. The little people? Buy the Freaking Dip! You Don’t Want to Miss Out!

Someone needs to be the bag holder.

Currencies

The buck de-confettied some more this week, rising 0.67 [+0.69%] to 98.20. It moved the weekly model back into an uptrend.

Losers: EUR [-0.52%], GBP [-0.59%], JPY [+0.92%], AUD [-0.88%], CAD

by acorn-endeavors

by acorn-endeavors