Consumer Economy

Retail Sales (RSAFS); $729B +3.3B (+0.45% m/m)

Industrial Production (INDPRO); +0.91% m/m

Producer Prices (PPIACO); +0.16% m/m

CPI All Urban (CPIAUCSL); +0.39% m/m

Retail Sales made a new all-time high, and it may be keeping up with inflation. Industrial production jumped higher – but it is not at a new all-time high. Still, the move is a positive sign, and not recessionary.

Producer prices (the old index, not the new one) didn’t change much. PPI is linked closely to energy.

Lastly, CPI rose 0.39%; annualized, that’s 4.68%. Since all the bureaucrats do is lie, this is an incredibly inflationary signal. Perhaps instead we should focus on “core CPI” (which removes the “useless” food & energy components – who needs them?), which rose just 0.23% this month, or 2.7% annualized.

Wolf’s take here:

Beneath the Skin of CPI Inflation: YoY CPI +2.9%, Worst since July, MoM CPI +0.39% (+4.8% Annualized), Worst since February. Core CPI Stuck for 7th Month at 3.1%-3.3%

(source – wolfstreet)

Wolf doesn’t sound so enthusiastic. My favorite indicator: “vaxxident” (motor vehicle) insurance, which was up “just” 0.4% m/m, but +11.3% y/y. Be careful out there.

Credit & Rates

Fed Balance Sheet (WALCL); 6.834T -19.5B (-0.29% w/w)

Total Bank Credit (TOTBKCR); 18.018T +72.18B (+0.40% w/w)

30 Year Mortgage Rate (MORTGAGE30US); 7.04% +11 bp

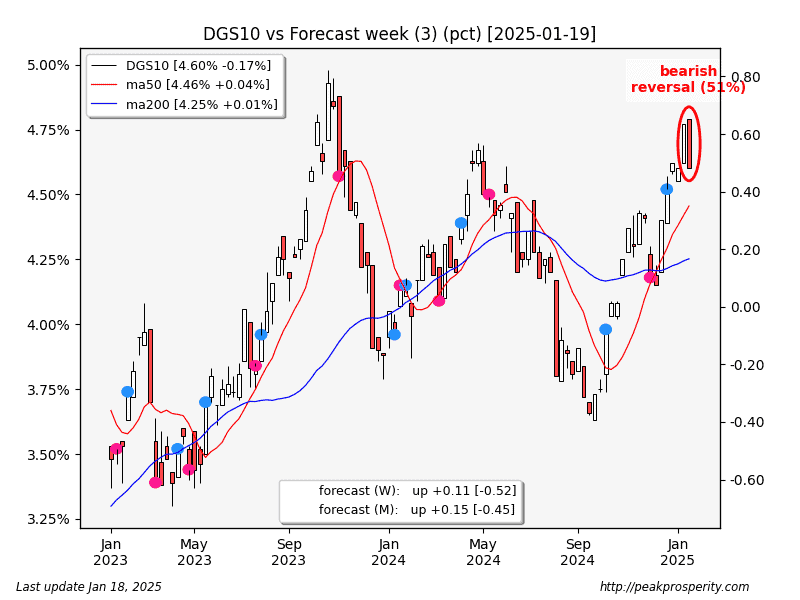

10 Year Treasury (DGS10); 4.61% -17 bp

We saw a massive expansion in bank credit this week, which hit a new all-time high. This increase erased all the deflationary-looking bank-credit contraction we have seen over the past two months. It’s not a very exciting chart, but if this week’s move happened every week for a year, bank credit would grow by 20.8%.

The 10-year yield (DGS10) fell 17 bp this week. The DGS10 candle print was bearish, but it has yet to change trend, according to my models.

In spite of the inflationary-looking CPI print, the bond market loved the CPI news; DGS10 shot lower, causing a rally in TLT. Oddly, SPX and JNK, and BTC all shot higher too, right at 08:30 Eastern on Wednesday, the time of the CPI release. I still am not sure why high inflation resulted in a bond market rally. Maybe “someone” really liked the “core inflation” numbers.

Overall, rates moved lower

by mike-from-jersey

by mike-from-jersey