This week we saw both a CPI and a PPI report, plus the usual suspects:

- Consumer Price Index (CPIAUCSL): +0.17% m/m, prior +0.18% m/m. Neutral.

- Producer Price Index (PPIACO): -0.26% m/m, prior +0.08% m/m. Deflationary.

- Fed Balance Sheet (WALCL): +1.47B w/w (+0.02%), prior -0.45% w/w. Neutral.

- Total Bank Credit (TOTBKCR): -35B w/w (-0.2%), prior flat. Deflationary.

While the CPI looks to be more or less where the Fed wants it to be (roughly 2%, annualized), and the PPI appears “deflationary”, bank credit is now in negative territory on a y/y basis, falling -0.17% this week alone. This is the first time bank credit has been negative on a y/y basis since 2009. This week’s plunge is pretty dramatic – annualized, it would be a 10% drop (52 * 35.8B / 17.2T). This is extremely deflationary.

Doing a deeper dive into bank credit, I looked at the components FRED provides here to see which areas are getting hit by shrinking bank credit. Long story short: banks have sold off or stopped buying/making Treasury Bonds (-7.6% y/y), Other Securities (-4.7% y/y), and Commercial/Industrial loans (-1.75% y/y), while they’ve modestly increased lending to consumers and real estate (roughly 2-3% y/y). Given the huge expansion in US Treasury debt, the fact the commercial banks are fleeing this market is bad for US Treasury yields, and the plunge in Commercial/Industrial lending looks bad for industry too. Even loan growth of 2-3% in the rest of the sectors isn’t great. I provide a chart of the values for “the rest” below – they are in dollars ($trillions). I know this is a lot of “inside baseball”, but – in the debt-based money system, the money supply must continually expand, or the interest on the debt cannot be paid – and not all sectors are being hit equally. Note the series below are updated w/w.

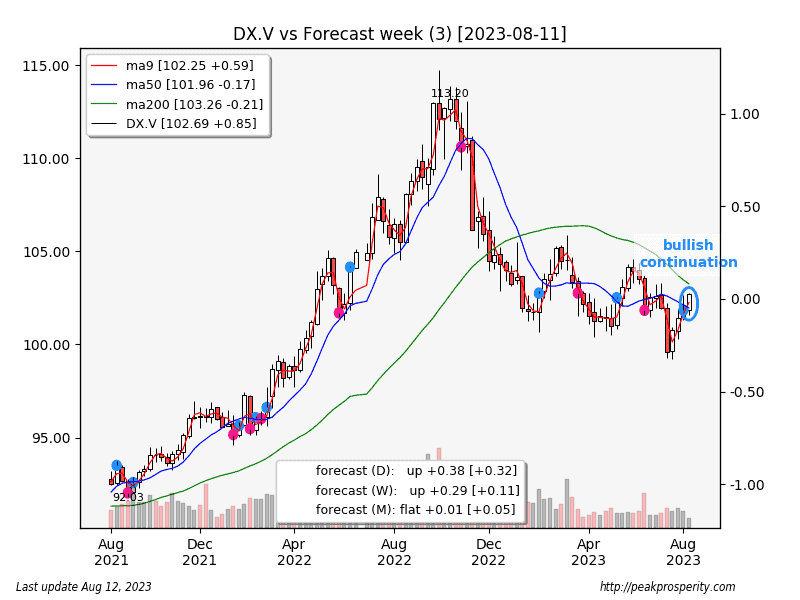

This week, the buck rallied strongly, up 0.85 [+0.84%] to 102.69, breaking back above the 50 MA. The buck has resumed an uptrend in all 3 timeframes, although the monthly uptrend is still very weak. The other sides of the trade did poorly: EUR: -0.83%, GBP: -0.67%, JPY: -2.20%, AUD: -1.8%, RMB: +0.96%. Note: for RMB, up is down.

We have that BRICS conference coming up in a few

by sand_puppy

by sand_puppy