For some reason, the equity markets in the US, Europe, and Japan are all ignoring the Iran war as if it weren’t relevant to their national economies.

Nothing could be further from the truth. However, Paul Kiker and I are seasoned enough to know that Western financial markets behave, shall we say, buoyantly during wars.

The robust upward price action in Bitcoin confirms that lots and lots of liquidity is suddenly finding its way into the markets. This looks, smells, and acts like liquidity-driven momentum, not a rational assessment of the risks.

If the “markets” were at all rational, they would not be having Japan, Europe, and the US moving in lockstep.

After all, Japan imports 100% of its oil and natural gas needs, while Europe is about halfway along that spectrum, and the US is nearly fully energy independent (at the moment).

In times past, there would have been distinct differences between those equity markets, and currently they are trading in lockstep.

Remember, oil is THE master resource. If you want more economic activity, then what you really want is more oil flowing into and through your economy.

With 10+ million barrels per day missing from the global economy, it’s a sure bet that the economy will shrink in 2026 if the oil flows are not rapidly restored.

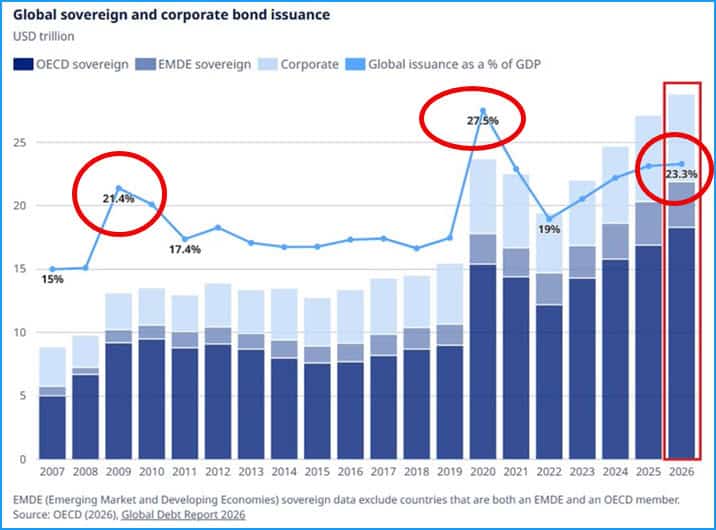

Against that backdrop, the projections are for sovereign and corporate debt issuance to hit the second-highest level as a percent of GDP over the past 20 years.

The projections call for 28 trillion of new borrowing, the majority of it ‘sovereign’ (meaning governments) in 2026.

Question: What happens if/when inflation comes roaring back due to wicked high energy prices?

Well, bond prices will fall, meaning bond yields will rise, and stocks will struggle too if history is any guide.

We also discussed:

- Food & beverage input costs jumped 373 bps to 7.9% YoY in March (driven by diesel/heating oil; fertilizer and plastics still to hit). Yikes!! Corn prices have not yet responded, but farmer input costs (fertilizer = ~40% of corn price) will force higher grain/protein prices later.

- The stagflation risk is rising: AI-driven layoffs are suppressing wage growth while supply shocks are pushing prices higher. 1970s-style environment likely — equities fell ~50% then despite rising corporate earnings.

- Historic Energy/Supply Shock Is Underway: The conflict has caused the largest energy disruption on record. Europe faces acute refined-product shortages; global commodities (jet fuel +60%, sulfur +53%, urea +49%, diesel/heating oil +46%) are surging. Markets are pricing the pain as “temporary,” but this is physics (not printable human folly) and will create sequential cost-push inflation.

- Trump’s Surprising Pivot: Trump stated he now favors higher interest rates to combat inflation (say what??), a sharp reversal from his prior “lower rates or markets collapse” stance.

- China’s Strategic Preparedness: China holds more strategic crude than the rest of the world combined. Perhaps coincidentally (or maybe not), China just recorded its highest-ever March silver imports (despite flat prices

The bottom line is that Paul is still advising prudence and caution while the cross-currents and competing narratives sort themselves out.

Timestamps

00:00 Market Dynamics Amidst Global Turmoil

18:42 The Shifting Economic Landscape and Inflationary Pressures

45:09 Market Reactions to Geopolitical Events

46:26 Oil Data Insights and European Market Dynamics

50:03 The Impact of Energy Supply on Markets

52:18 Understanding Market Behavior and Risk Management

53:47 The Importance of Energy in Economic Stability

56:42 Current Oil Inventory Trends and Future Implications

59:18 The Role of Algorithms in Market Trading

01:03:26 China’s Strategic Position in Global Oil Supply

01:07:57 China’s Silver Imports and Economic Strategy

01:12:10 The Concept of ‘Magic Money Machines’

01:17:59 Modern Monetary Theory and Its Implications

01:19:19 Emotional Decision-Making in Financial Planning

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.

by mike-from-jersey

by mike-from-jersey