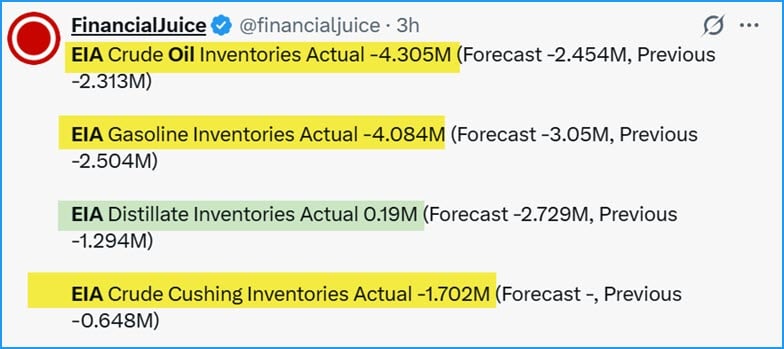

Last week, according to the EIA, the US continued to aggressively export its crude oil and gasoline stockpiles.

When we add the 8.6 million barrels withdrawn from the Strategic Petroleum Reserve (SPR) to the 4.3 million barrels drawn from commercial stocks, we find that a total of 12.9 million barrels of crude were removed from the national stockpile and exported to the world.

While this serves to temporarily blunt the observed global price for crude oil and gasoline, it creates the conditions for much higher future prices in the future.

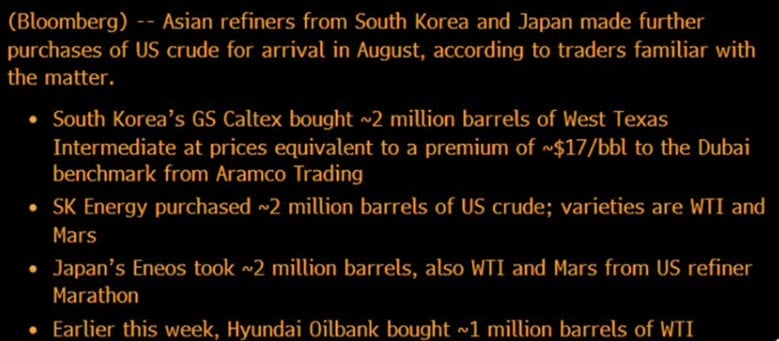

Where did they go? Well, Asian customers alone bought another 7 million barrels of US crude oil for an August delivery:

We’re eating (and selling) our seed corn.

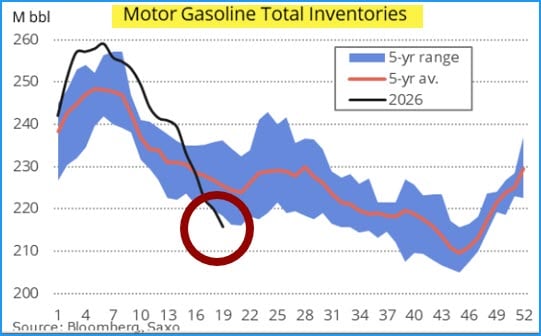

Relatedly, US gasoline stocks are also being exported and are now well below their five-year average and screaming lower right before the US summer driving season:

What happens next is obvious – US gasoline prices are going to rise, and probably by a lot and soon.

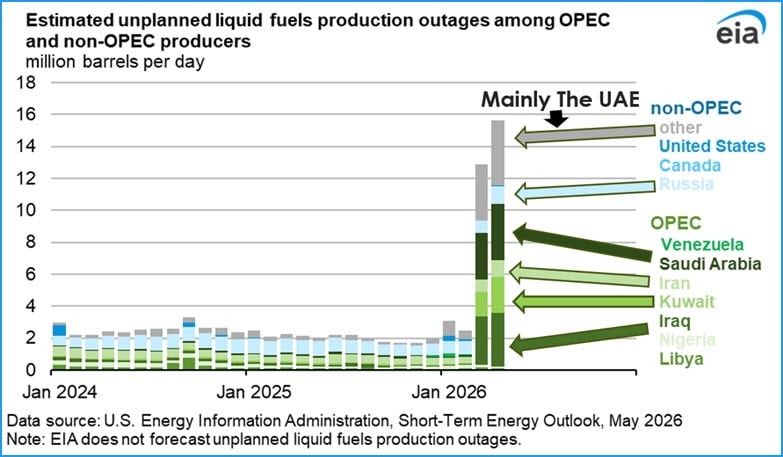

One possible reason global stocks are being drawn down so far and so fast is that the unplanned disruptions to oil production have been larger than first thought. On that front, the US EIA put out this chart showing a nearly 16 Mb/d disruption for April, far higher than the oft-quoted 10-11 Mb/d figure.

The above chart is “all liquids,” so that means the various refined products that are also not leaving the Persian Gulf, besides just crude oil.

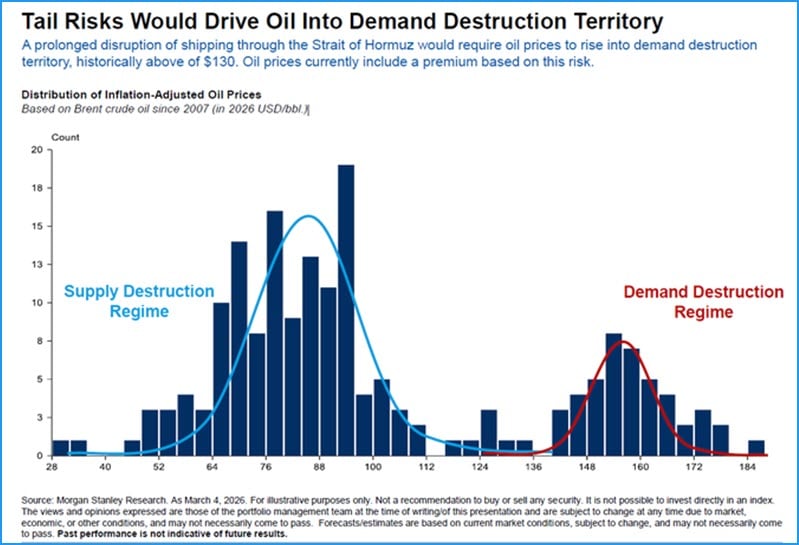

But the big problem the world is facing, now exposed by the Iran War, is that the price that oil companies need to turn a profit on new wells is marching toward the price that a debt-addled world can maximally afford to pay for oil.

Someday, when the blue hump converges with the red hump, it will be game over for the system of perpetual debt expansion, which far too many politicians and bankers think is an untouchable divine right of theirs.

The bottom line is that every single day that the Strait remains closed is another day of damage being done to the economic superstructure.

Are you prepared?

by friday

by friday