NOTE: The Renaissance Report is presented as a fully written piece and as a video recording. Each version can stand alone so that everyone can consume it in their desired format. The video is at the bottom of the write-up.

Setting The Stage

Introduction: We’re living through one of the most dangerous but also potentially rewarding periods of time. Great family fortunes will be made or lost over the relatively few years. A great wealth transfer is underway, and whether you are on the winning or the losing side of that story depends on the exact investment decisions you will make. Today, no decision is a decision. Standing aside and hoping for the best is a guaranteed losing strategy. In the Renaissance Report, I will provide a root-cause analysis of why certain things are unfolding, so you can make better decisions about what to do. In other words, my method involves revealing the “why” before presenting the “what.” It all begins with this thing we call “money.”

Okay, folks, I have officially hit “that stage” of life. I have some big ideas in my head, and either I get them out now, or I might never get it done. It’s now or never, right?

After nearly 20 years of analyzing the world’s events and economic history, and then communicating my findings to my audience, it’s now time to shift gears a bit.

The Renaissance Report assumes nothing. Some of you know me well; other people are here reading or listening to me for the first time. Some of you will hear old, familiar ideas, and others will be exploring these ideas for the first time. Even if you are one of the ‘old hands’, I invite you to listen to everything all over again, because the material will probably settle in deeper this time, find new landing spots in your mind, and invigorate new ideas and thinking.

Until 2026, I was in ‘react and scramble mode’, constantly pulling from the most recent events to help people stay oriented to what the current events were telling us about where we were/are on the timeline. Now, I am going to be doing deeper dives into the subjects.

One of my top goals is that you become even more resilient than you already are. If I do my job well, each Renaissance Report will be a clear and clean signal that both reveals something new about where events are headed, and what you can do to prepare for events or profit from the insights.

Welcome to Volume 1 of the Renaissance Report.

Introduction

I’ve been an economic and resource analyst and a writer/author/video communicator for 20 years. My very first blog was “Dr. Martenson’s Straight Story,” launched in 2006 to warn people about what I thought was a housing bubble. I was heavily short that particular bubble at the same time as the characters in the movie “The Big Short.” I had more than a passing interest in the tale.

That soon became ChrisMartenson.com for 2007-2008, and then finally my efforts became the Peak Prosperity website in 2009. The rest is history. My first forays into what eventually became The Crash Course were public presentations held in 2007 and 2008 called “The End of Money.”

What a strange title, right? That’s a bit of foreshadowing.

My background includes a B.S. in Natural Science from Lewis & Clark University in Portland, OR, a Ph.D. in Pathology from Duke University, and an MBA from Cornell University with an emphasis on finance. Right out of my MBA program, I worked for 3 years in corporate finance at Pfizer’s R&D division in Groton, CT (beginning in 2001, it didn’t work out between us). Then I was a VP at a company called SAIC. Then I went on to work with people I loved and trusted during the dot-bomb stage of things, learning more from those failures about business than I could have after 100 years with either large company in my past.

But in 2005, I lost my mojo for working for anybody at all, and so I began investing actively, day trading stocks and futures (mainly gold), and I started that first blog in 2006. By 2008, I had created my signature piece The Crash Course, which synthesized the topics of the economy, energy, environment, and exponential growth at the systems level.

It should have been a complete dud, because it was some guy (me) merely speaking over PowerPoint slides in 20 chapters initially that took ~3 hours to wade through. But it was wildly successful and became a book, an updated book, and an updated video series that is now patiently awaiting me to have enough time to update it again.

Along the way, I gave talks all over the world; in the UK Parliament, in Madrid, on PBS Newshour, at Peak Oil conferences, and at the Commonwealth Club, to name but a tiny handful.

Look At That Handsome Young Guy!

(Source)

I’ve written about silver more than 250 times. Gold, pretty much weekly except for those weeks when it was daily.

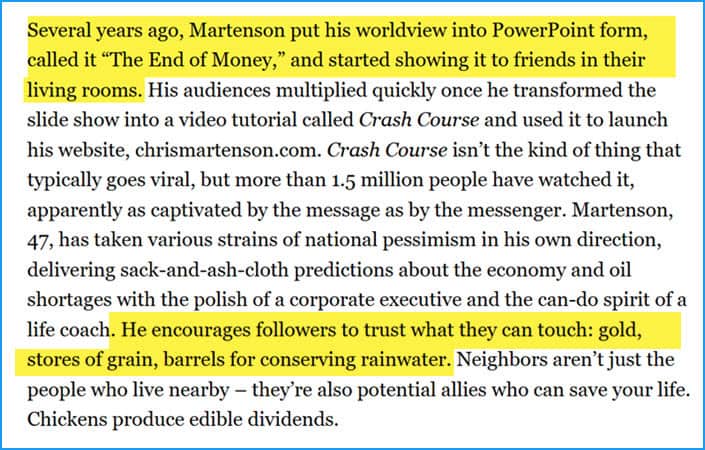

My first ‘hit piece’ came out in 2010:

They sent a full photographer team, and spent 3 days with me, hearing all about how the economy, energy, and environment came together into my view of how things might progress. Naturally, they photoshopped me into a bunker, with a chicken.

+

+

I wonder if they’d like a chance to revisit this framing?

The entire time I’ve been as fierce a critic of the Federal Reserve (calling them “financial terrorists” as early as 2008) as I have been a strong advocate for owning gold and silver and other hard assets.

My instinct is to deep dive into the raw data and precise mechanisms that drive our financial systems. When the data changes, I freely and easily change my points of view and opinions. Along the way, I’ve consumed an enormous variety of opinions by a great many commentators and analysts, often on the fly as I conducted hundreds of podcast interviews with truly amazing people.

Perhaps the largest portion of my success is due to the fact that I learned how to listen carefully to others, having eventually figured that when I was talking, I wasn’t learning. My approach is to combine insights from extremely disparate fields into a cohesive and coherent understanding of how the world works.

Making predictions is hard, especially about the future.

~ Yogi Berra

I don’t make predictions so much as I extrapolate current trends and conditions into the future. Central to getting so much right over the years was finally coming to terms with the idea that people are gonna people. Meaning, the best way to “predict” the future is to toss out all the elegant analyses and just study how people have always behaved throughout history and then assume that’s what they’re going to do again today and tomorrow.

In short, most people, especially those in authority or political positions, are going to lie, cheat, rationalize, do every wrong thing before finally doing a right thing, and always, always, always kick the can down the road until there is no more road left.

Discouragingly, they will then write self-congratulatory books with multi-million-dollar advances for having the courage to print.

The rest will hand out awards to each other for being such swell folks.

I’ve been wrong many times, particularly about timing. Things often seemed more imminent than they actually were. Everything has taken far longer than it “should have” to finally change. I chalk this up to most people being rationalizers, not rational. The slow pace of actual change has tempered me over the years.

Back in 2008, when the first video version of The Crash Course came out, I said:

“The next twenty years are going to be completely unlike the last twenty years.”

That might seem unhelpfully vague and broad, but I understood two things; (1) the sort of global topping process we were going to undergo would take a long time to play out (but will seem like the blink of an eye when people look back from a hundred years hence) and (2) the twin afflictions of “recency bias” and stubborn belief systems would make real progress difficult.

More on both of those and other psychological and belief systems in later reports.

Still, in hindsight, seeing what we’re now facing and likely to face by 2028 when my window of warning will expire, I think that is going to prove to be a dead-nuts-on call. But perhaps I just got “lucky.”

I did have a nearly three-year detour from economic and resource topics brought about by Covid and my analyses and guidance were of immense help to a lot of people. But the style was the same; dive in, figure out what the truth was, and share it without any regard for whether or not that would make me more popular on social media (it did not) or piss off future potential advertisers (it surely did).

If you are one of the people who started following me then, these economic and resource-focused Renaissance Reports aren’t the departure from my core mission; Covid was. I would strongly encourage you to stick around because, if you didn’t like the 99.95% survival rate of Covid, you are positively going to be terrorized by the social and cultural disruptions that will erupt once we have to collectively confront the degree to which we mismanaged our monetary system and ‘forgot’ to invest in the future.

That’s a very short tour of who I am, how I approach things, and what I’ve been up to for the past 20 years. I felt it necessary to explain that I am not a Johnny-come-lately who watched a few TikTok videos about money and metals and then decided to talk about them.

The Birth of Money

Before we get into the foundational topic of “The End of Money,” we have to begin with The Birth of Money. How does money come into being? How does it disappear later on? Who decides how much should be created?

This is a subject of vast ignorance within and across Western cultures. Not because it’s especially difficult or complicated, but because the authorities within those cultures have gone out of their way to prevent the topic from being taught or discussed.

My introduction began when I read The Creature From Jekyll Island (G. Edward Griffin) in 2001, and so I was able to articulate the process clearly back in 2008 in The Crash Course.

In there, we learned that banks create money when they make loans.

Here’s a 2025 interview between Tucker Carlson and the economist Richard Werner explaining the process:

How hard was that? Not very. Banks create money when they make loans. That’s it. That’s the whole system. When you ‘borrow’ $300,000 from the bank to buy a house, they simply click on a few keys and – presto! – you have $300,000 of spending power, as well as a $300,000 debt obligation to the bank.

If you fail to pay back even a single month’s mortgage payment, you could lose your entire house to the bank. Honestly, when you think it through, it’s a form of debt-slavery, but that’s another insight to explore more deeply another day.

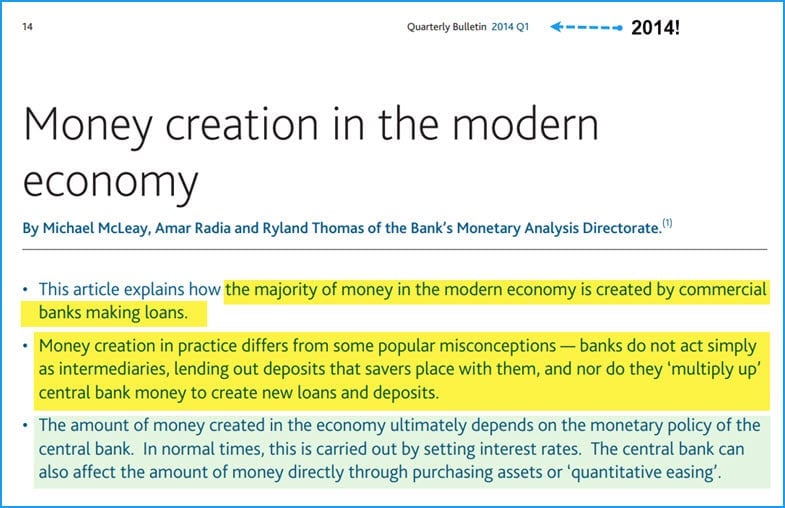

Imagine my surprise when the Bank of England excitedly revealed in 2014 that they had discovered the same thing!

What does it mean that the research staff of the Bank of England took until 2014 to ‘discover’ that banks create money in debt-based fiat money systems? It means that this very obvious feature had been studiously and consciously scrubbed from the lesson books by people who very much wanted to conceal this feature from the public. To do so, they had to first conceal it from themselves.

So, let’s dig into this very bland-sounding but quite extraordinary series of admissions by PhD economists at the Bank of England:

“The majority of money in the modern economy is created by commercial banks making loans.

Not “some” but “the majority.” This is obviously a very important insight. Why? Because the flip side of credit creation is money creation. When a loan is made, an offsetting amount of money is created.

“Banks do not act simply as intermediaries, lending out deposits that savers place with them, and nor do they ‘multiply up’ central bank money to create new loans and deposits.”

Yes, you read that right. Banks do not need deposits, nor do they need freshly printed hot (“QE”) money from the Fed to lend out. They simply make loans whenever they wish and in whatever amounts make sense to them.

Commercial banks, not the Federal Reserve, are the beating heart of this system. The Fed cares not one whit about “price stability” or “full employment.” Those are retail slogans designed to provide weak cover for the Fed’s one and only true mandate, which is to keep commercial credit expanding.

How can we detect this for ourselves? Easy.

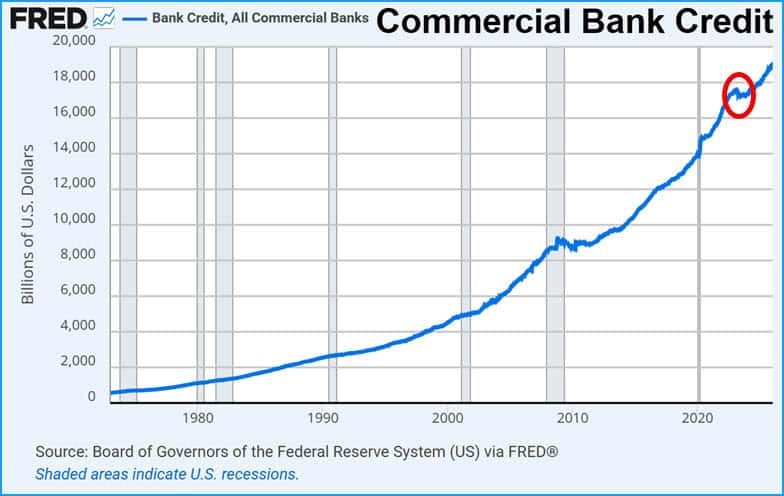

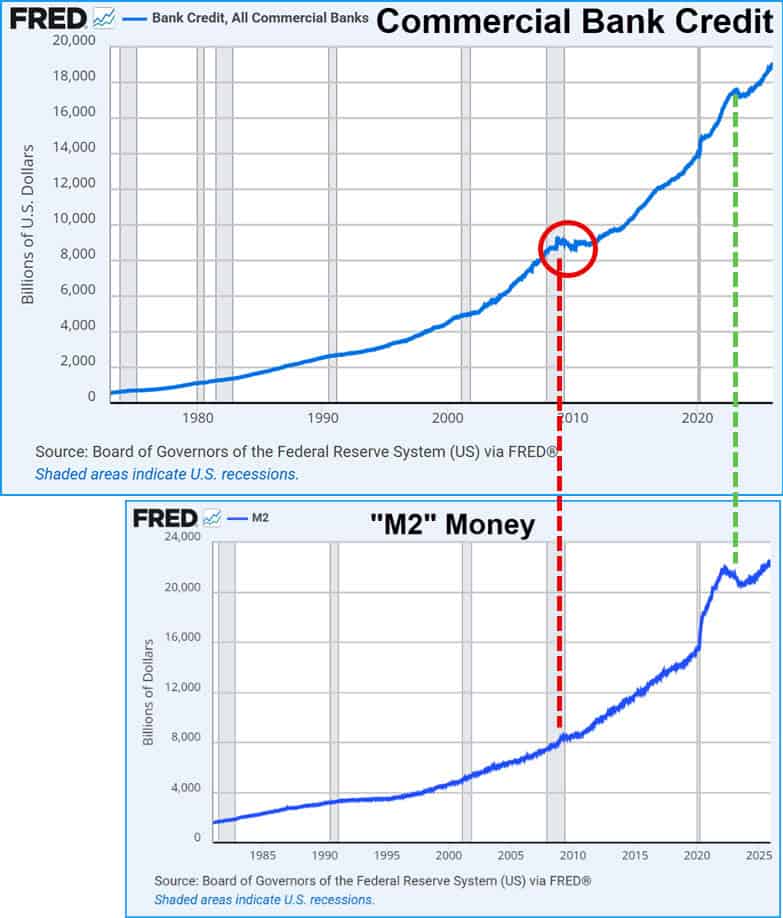

First, we look at the total amount of loans made by the commercial banks:

I’ve circled an important moment in time in red, which we’ll get back to shortly.

Now we compare that to “M2,” which is the broadest accounting of ‘money’ in the US banking system we have left (after the Fed stopped collecting and reporting the far more important and much broader “M3” measure on March 23rd, 2006).

There’s a pretty good, but not perfect, alignment there in keeping with the idea that “the majority” of money (M2) is created by commercial banks making loans (let’s call that “commercial bank credit” or CBC so I don’t have to type so many letters going forward).

Here’s a stacked view of those two charts so we can better appreciate the dynamics at play. Sorry for the different sizes, I had to shrink one a bit to get the years to stack perfectly.

First, in the red circle is the Great Financial Crisis (GFC), where we can see that CBC not only stopped growing exponentially, but actually went sideways and even backwards for 6 quarters. That, my friends, nearly collapsed the entire banking and related financial systems of the U.S. and the world.

Too bad the professional economists and regulators of the day were completely unprepared to understand what had happened and why:

So, here’s our first powerful insight…if and/or when bank credit stops growing, the entire financial ecosystem threatens to implode. Like a shark that needs to keep swimming to stay alive, a financial system built on debt-based money must constantly expand.

The second insight comes from 2022, where, in response to the Federal Reserve hiking interest rates, M2 fell first and fastest (green dotted line), and CBC followed suit shortly thereafter, but not nearly as dramatically.

Still, what was the effect on the financial markets of these short-lived declines? 2022 was an UGLY year with both stocks and bonds.

So you can imagine the many incentives the Fed has to keep the system of money expanding rather than contracting.

For reasons too numerous to get into here, if loans are not growing at a pace fast enough to both pay back all the outstanding principal amounts plus the accumulated interest, then the financial system ‘experiences stress’ which is a euphemistic way of saying “threatens to collapse and plunge us all into cannibalism and a multicentury new Dark Ages.”

Okay, some hyperbole there on my part, but the Fed, Wall Street, and politicians act as if that were actually the case.

The main point here is that the entire ‘program’ that the Federal Reserve is enabling is contained in the phrase “Inflate or Die.”

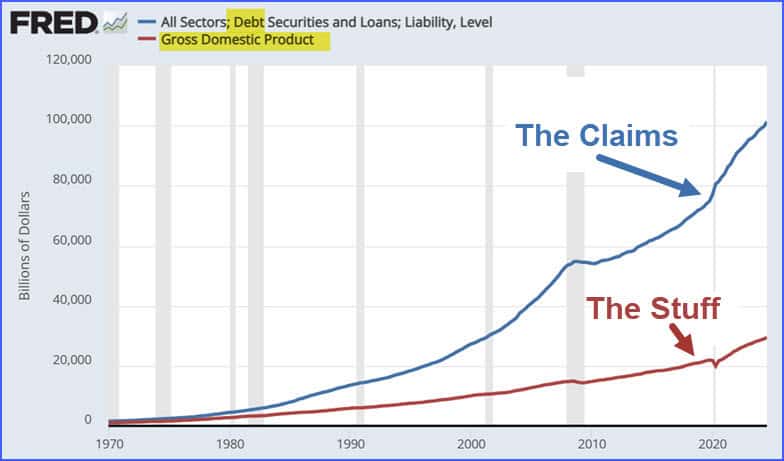

Over time, at a macro scale, this is what it looks like for the U.S., comparing total debt (including federal, state, municipal, corporate, and household) to GDP (which is the ‘stuff’ that all those debt claims are set against):

Once again, nobody in any position of fiscal or monetary authority has bothered to explain how you can constantly pile up the claims (debt) at a faster pace than the stuff (GDP) forever. The reason they haven’t? Because the answer is ‘austerity,’ which is both politically unpalatable and systemically devastating.

Summary: Money is ‘born’ when a loan is made. It disappears when the loan is paid off. Because the interest isn’t created with the loan, a dynamic of perpetual expansion of debt/credit is a feature of the system.

Understanding both the “hows” and the “whys” of the birth of money allows us to then have a proper discussion of The End of Money.

What Is Wealth?

Before we dive into The End of Money, we’ve got to take a quick detour into the question of “What is wealth?”

This seems like a trite question because the usual answer to “Who is the wealthiest person you know?” is whoever has the most currency and financial assets in their bank and brokerage accounts. These forms of wealth are what I call ‘tertiary’ and are themselves dependent on ample streams of primary and secondary forms of wealth.

What do I mean by that?

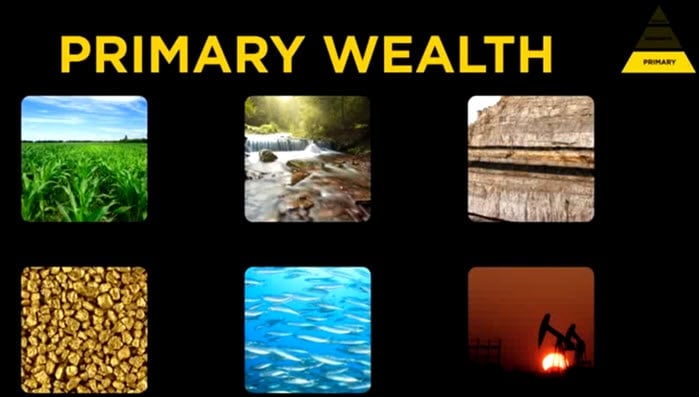

Primary wealth consists of the raw resources of the land. It is thick coal seams, teeming fishing grounds, and rich soils.

If you have these things in your country, then you have the basis for creating a prosperous nation.

Moving up the pyramid, we arrive next at secondary wealth, which is primary wealth brought to market. You can also think of this as ‘the means of production.’ Secondary wealth is trees converted into lumber and brought to market. It is food grown and then brought to market. It is iron ore converted into steel pipe.

There’s a hidden rule sitting between these two forms of wealth; without primary wealth, there cannot be secondary wealth. No coal in the ground (primary) means no coal sold to a steel furnace (secondary). No trees means no lumber. No oil in the ground means no gasoline at the pump, etc., and so forth.

Primary wealth is a necessary precondition for secondary wealth.

Which brings us finally to tertiary wealth. This consists of money in the bank, Treasuries held in brokerage accounts, and every single derivative – all $2 quadrillion (with a “Q”) of them.

Tertiary wealth usually has no tangible or intrinsic value on its own. It’s digits on hard disks, words on a derivative contract, or paper in a wallet.

And just like secondary wealth rests upon primary wealth being there in the first place, tertiary wealth relies on the prior two forms.

And this is where the trouble starts.

When Money Dies

Now we get to the heart of it all.

…

by cmartenson

by cmartenson