Executive Summary

- Why pressures to the downside have less impact when the global economy is weak

- Why oil's new floor is $80

- The 'upside risk' story for oil prices

- Why prices will march up to the $150-175 range over the next 2-4 years (with increasing sensitivity to spikes of over $200+ per barrel)

If you have not yet read Part I: The Repricing of Oil, available free to all readers, please click here to read it first.

I encourage others to read the entire recent paper on Nominal GDP (NGDP) Targeting by Michael Woodford (recently delivered at Jackson Hole) or to simply read its coverage, either by Joe Weisenthal at Business Insider or Paul Krugman at the New York Times. In short, I take the appearance of the Woodford paper (link opens to PDF) as the inevitable next-step solution to the problem of unpayable debt and scarce resources. By loudly and flagrantly voicing a policy pursuit of inflation, Nominal GDP Targeting (which has been discussed for some time in economic circles) would be the next iteration of behavioral prodding in Western economies.

More importantly, the growing acceptance of NGDP targeting in policy circles simplifies the battle that began a decade ago: the struggle to counter emerging scarcity of natural resources with the provision of greater and greater amounts of cheap credit. Within the contours of this battle lies the answer as to whether oil’s next major move is downward, in a deflationary collapse, as global demand vanishes in a new economic crisis; or whether oil’s next major move is higher, as the five billion people in the developing world pull the OECD along in a new expansion.

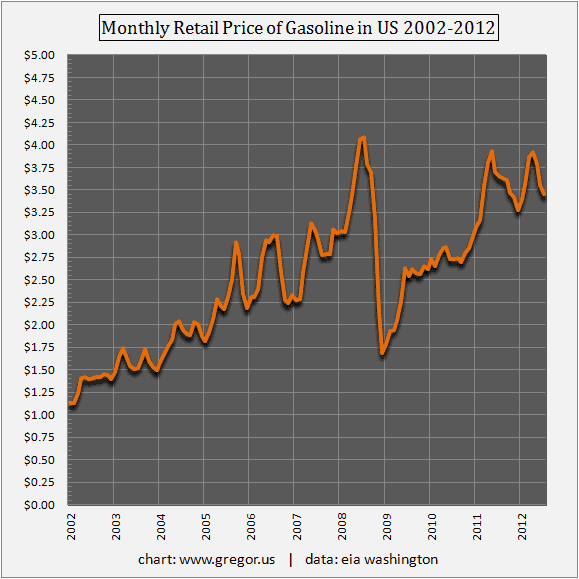

Modeling the next move in oil prices is, of course, a very different task than it was ten years ago. Back then, credit growth through normal channels was still possible and the limits to increases in oil production were more well-defined. It was an easier call that the global economy would easily push forward in a straight line until the cheap oil ran out, and then bang! We hit a wall. That is why the shape of the price advance was sustainably incremental and then resolved in a super-spike.

Here is a ten-year chart of monthly retail gasoline prices in the U.S.:

Counterintuitive

Naturally, we are inclined to say that the next move down in oil prices will come

by cmartenson

by cmartenson