The risk faced by those who are analyzing macro trends is sounding like a broken record. For those younger readers who have no idea what that phrase means, imagine an mp3 song that will stick on and endlessly repeat a random segment of the song you are listening to until you give your device a sharp knock on the side. That’s what a broken record sounded like.

The risk faced by those who are analyzing macro trends is sounding like a broken record. For those younger readers who have no idea what that phrase means, imagine an mp3 song that will stick on and endlessly repeat a random segment of the song you are listening to until you give your device a sharp knock on the side. That’s what a broken record sounded like.

The world economy is on the ropes, and it won’t ever recover, at least not to anything resembling its recent past. Neither the gleeful housing bubble nor the free-flowing credit that enabled that side bubble to emerge will return. The resources simply do not exist to repeat that final orgy of consumption. A new reality is upon us, and while — fortunately — more and more people are choosing to face our predicament rather than pretend the current risks and challenges do not really exist, the absolute numbers of such forerunners are still small, and for the most part they don’t include any of our political leaders.

The macro trends of worsening public and private debt loads, a looming and unaddressed Peak Oil threat, exponentially increasing global population, resource depletion, and an all-too-human tendency to use the money printing machine to deal with tough economic problems all remain pointed firmly towards an uncomfortable conclusion: There’s a future of less in store for most people.

Our best hope is for a negotiated decline to lower levels of economic activity that allow us to gracefully adjust our expectations to a new and lower level consumption that offers an even more enjoyable and purpose-filled existence. Our worst fear is that a stubborn insistence on business-as-usual by our leadership leads to a future shaped by disaster rather than design.

The fundamental issue is this: You can’t solve a problem rooted in too much debt with more debt. It just doesn’t pencil out.

“Here we go again…solving a debt problem with more debt has not solved the underlying problem. …Can the US continue to depreciate the world’s base currency?”

~ Goldman strategist Alan Brazil (Source)

Yet we now see that both Europe and the US are busily conceding to banker demands and coming up with all manner of fancy schemes, in an attempt to hide the fact that old debt is simply being replaced with new debt.

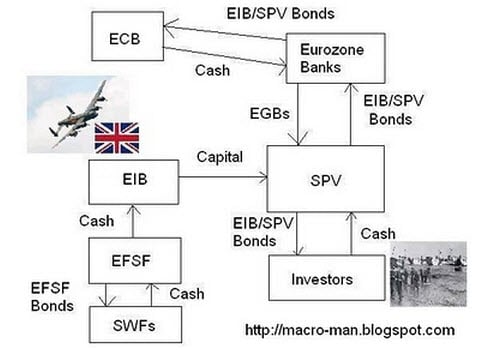

Consider the confusing news about the European EFSF, the so-called rescue facility for the Eurozone, which is currently conceived to use leverage (to solve a debt problem!) and is thought to look something like this:

We could analyze the details of that flowchart and opine on the structure, but that really won’t aid anything. Additional complexity and Jell-O redistribution will not change the basic fact that the debts simply cannot be paid back under current terms or out of any imaginable future economic growth.

As far as I can tell, the complexity serves one main purpose, and that is to baffle enough of the populace for long enough to allow a significant transfer of public wealth to occur in broad daylight into private pockets. In this regard, Europe and the United States seem to be identical.

A Bad Reaction

On September 21, 2011, the Fed disappointed the world equity and commodity markets by announcing Operation Twist, which is nothing more than monetary Jell-O being moved from one side of the plate to another, instead of more QE stimulus (representing additional Jell-O in this metaphor).

The reaction was swift and negative.

Beginning with stocks, we see that a couple of severe down days (the red bars in the green circle) ensued, following the Operation Twist announcement.

We also note that the S&P 500 is down year to date (YTD, blue dotted line) and that it is bouncing between the 1120 and 1220 marks (purple lines) with a lot of volatility but not much direction. The simplest explanation for this is that tensions exist between what the fundamental data is telling us about the state of the global economy (not good; more below) and the hope that more central bank money will soon be flooding the world.

As always, this is not a good sign. Any time you read the word “investors” being used in an article about who is driving these price movements, I invite you to replace that word with “speculators,” as that’s what we all are now. We are left speculating wildly about when and how much thin-air money will next be injected by one central bank or another.

Gold had particularly tough going after the Twist announcement, getting clobbered for ~$100 on the following couple of days (green circle):

These price drops had nothing to do with an improved outlook on the viability of the world’s fiat money systems or a reduction in overall systemic risk. Neither were appreciably altered by the Fed decision, although systemic risk was probably elevated. Without the Fed absorbing additional existing debt, the entire system is at greater risk of slipping into a deflationary spiral that could get out of control.

If that happens, you want to be sure to have gold — in hand.

Silver was especially slammed and was the undisputed loser of the entire commodity complex, losing as much as 25% in a single session (before recovering):

I have always held that the risk for silver in this current rout would be for it to behave more like an industrial metal than a monetary asset, and therefore slip in price regardless of systemic stress. For a while there, throughout July and August, I began to think that silver was displaying some money-like qualities, but the recent slam dispelled those thoughts.

I continue to think that this rout is not yet over and am waiting on better prices for silver before I remove some of my dry powder and accumulate some more.

The ‘off note’ in this story is the price of oil:

Until and unless oil, the main lubricant of commerce and a feed-in to the price of everything, slips and plummets a long way from here, I remain bullish on commodities in general. The macro story for oil is simply that a marginal new barrel of oil costs at least $70 in today’s world, and quite a bit more in some cases.

If oil falls below that $70-$80 level, then you can forget about new supply coming on line. In many respects, we are living in an ‘oil shadow’ created by the plunge in oil to $38 in 2009, which delayed a large number of oil development projects that would otherwise be yielding supply today.

Should oil fall below the marginal cost again here in 2011 or 2012, then we’ll have another oil shadow to contend with a few years down the line.

Of course, I should point out here that the above chart is for US oil only (WTIC) and that the world price for oil is roughly $20 higher, as indicated by the price of Brent crude at $104/bbl.

Slip-Sliding Away

Presently, the global economy is not doing all that well. There are troubling signs from Japan, the US, Europe and now China that the economy is stalling out and in serious danger of slipping back into recession. If that happens, all of the debt-rescue plans will have both additional headwinds with which to contend and new debt implosions to rescue.

Any analysis of the global economy has to begin with Dr. Copper, the most trusted source for an accurate economic diagnosis. Used in an enormous variety of commercial applications, from houses to cars to electronics to electricity cables, copper prices usually provide a useful early read on the direction of the economy.

That tale is one of weakness:

Copper prices are now back to where they were in 2008, although still considerably up off the lows of late 2008 and early 2009, and are in negative territory YTD by more than 20%.

Consistent with the weakness in copper prices are recent reports of Chinese manufacturing activity slipping into contraction:

China manufacturing data paint weak picture

(Sept 22, 2011)

HONG KONG (MarketWatch) — HSBC’s preliminary China Manufacturing Purchasing Managers’ Index, or “flash” PMI, fell to a two-month low in September, indicating a broadening slowdown in the Chinese economy, with industrial output swinging from a modest expansion to a deterioration.

The weak data were a factor in the broad equities sell-off in Hong Kong Thursday.

The headline preliminary PMI for the month was 49.4, down from 49.9 in August, HSBC said in a statement Thursday.

The PMI’s output index fell to 49.2 in September, down from 50.2 in August and below the 50 level dividing expansion from contraction.

China is addicted to rapid rates of growth, and its banking system is heavily exposed to a wildly over-priced real estate market, especially in their major urban centers. If the Chinese property bubble busts, then expect major banking stress to follow suit.

Perhaps one nearby indicator is the health of the Hong Kong real estate market, which is now entering a dangerous phase:

Hong Kong’s Tsang Sees Property ‘Soft Landing,’ Backs Peg

(September 27, 2011)

(Bloomberg) — Hong Kong Financial Secretary John Tsang predicted a “soft landing” for the real estate market and said the city will keep its currency peg to the U.S. dollar, blamed for helping drive home prices up about 70 percent.

“The residential market has basically frozen as a result of the curbs and the global downturn,” said Alva To, head of consulting for North Asia at DTZ, a property broker. “Our surveyors are seeing almost a 60 percent drop in the number of valuation queries from banks compared with normal times.”

Hong Kong’s used home sales have slowed, with prices falling for the first time in seven months in July. That’s not a “very violent reaction,” Tsang said. Prices have jumped about 70 percent since the start of 2009. New loans approved fell 10.3 percent in August from a month ago.

A 70% jump in prices in two years is not a healthy sign; it is an indication of a bubble. The basic trajectory is simple enough; falling sales then lead to falling prices. Once the dynamic is underway, it will not stop until prices again reach affordability for the median household (at best) and may even badly overshoot to the downside (at worst).

More directly, Chinese real estate developers are encountering a slump in both sales and prices:

China Developers Face More ‘Severe’ Credit Outlook, S&P Says

Sept. 27 (Bloomberg) — Chinese developers face an “increasingly severe” credit outlook, which may force them to cut prices and turn to costlier funding sources as sales weaken, Standard & Poor’s said.

A 30 percent decline in sales may leave many developers facing a liquidity squeeze, S&P said after conducting stress tests of the nation’s real estate companies. Most developers would be able to “absorb” a 10 percent sales drop next year, the credit rating company said.

“The worst isn’t over for China’s real estate developers,” S&P analysts led by Frank Lu wrote in a report today. “Developers are bracing themselves for slower sales and lower property prices ahead.”

Fewer than half of the 70 cities monitored by the government in August posted month-on-month gains in home prices for the first time, according to Samsung Securities Co.

What will happen to Chinese lending to the US and Europe if global trade slumps and the Chinese banking system begins to experience severe stress as a consequence of their own real estate bubble popping? Probably nothing good. That’s why we have concerns that the enormous bubble in US Treasuries may be exposed as early as next year (2012).

Consistent with the rumblings from Dr. Copper are the reported slumps in global trade recently hitting the wires:

German Exports Unexpectedly Fell in July

(Sep 8, 2011)

German exports unexpectedly declined for a second month in July, underscoring signs Europe’s largest economy is losing momentum as the global recovery falters.

Exports, adjusted for work days and seasonal changes, fell 1.8 percent from June, when they dropped 1.2 percent, the Federal Statistics Office in Wiesbaden said today.

German growth is slowing as Europe’s debt crisis prompts governments from Spain to Ireland to cut spending, sapping export demand. Factory orders from abroad dropped in July and executives and investors grew more pessimistic last month. Bayerische Motoren Werke AG (BMW), the world’s biggest maker of luxury cars, said on Sept. 1 that U.S. sales dropped in August.

Japan exports disappoint, could weaken further

(Sept 20, 2011)

TOKYO, Sep. 20, 2011 (Reuters) — Japan’s exports rose in the year to August at less than half the pace expected as a global economic slowdown, a strong currency and Europe’s sovereign debt crisis put Japan’s own recovery increasingly in doubt.

“The impact of a slowing in the global economy is starting to become visible in Japan’s export figures,” said Takeshi Minami, chief economist at Norinchukin Research Institute.

“In the coming months exports may go back to posting year-on-year declines, meaning the economy will have no sufficient support factor unless the government quickly implements reconstruction spending.”

[US] Economic indicators predict continued weak growth

(Sept 22, 2011)

[F]actory orders, unemployment benefit applications and hours worked were among six measures that weakened in August.

Existing home sales up but price outlook grim

(Sept 21, 2011)

WASHINGTON (Reuters) – Existing home sales rose in August to their highest in five months as lower prices and rock-bottom interest rates drew more buyers into a still moribund market.

Sales climbed more than expected, up 7.7 percent from the previous month to an annual rate of 5.03 million units, the National Association of Realtors said on Wednesday. The median price was 5.1 percent lower than a year earlier.

Existing home sales have trended lower in 2011 and prices are still weakening. One factor keeping prices low is the high rate of “distressed sales” which include those forced by foreclosures.

Distressed sales accounted for 31 percent of August transactions, up from 29 percent a month earlier.

Comment: Note that falling prices are not a good sign here. Also the 7.7% bump in sales, assuming we believe the NAR data (always worth taking it with a grain of salt), still leaves us well off the peak of several years back and is being driven in large measure by distressed sales.

Let’s contrast the distressed bargain activity with new home sales, also for August, to see if a different picture emerges:

New home sales fell in August for 4th month

(Sept 26, 2011)

Sales of new U.S. homes fell to a six-month low in August.

The fourth straight monthly decline during the peak buying season suggests the housing market is years away from a recovery.

The Commerce Department said Monday that new-home sales fell 2.3 percent to a seasonally adjusted annual rate of 295,000. That’s less than half the roughly 700,000 that economists say must be sold to sustain a healthy housing market.

New-homes sales are on pace for the worst year since the government began keeping records a half century ago.

New home sales are on a pace for the worst year since records began fifty years ago? That statistic alone should tell you exactly where we are in this so-called recovery. Absolutely nowhere. The decline in new home sales wipes out the warm glow from the increase in existing home sales.

Summary: Part I

The world that Europe, the US and Japan are desperately trying to sustain is no longer possible in a world of too much debt and too expensive energy. The plethora of sliding data noted above represents classic warning signs taht one would expect to see from a global economy in systemic decline.

We are now down to the wire. Over the next few months and years, our story of credit growth – four decades in the making – will continue to unwind. Those who place their faith in the authorities to first, understand the true nature of the predicament, and second, implement restorative policies, are at tremendous risk of personal and/or financial losses.

In Part II of this report: Understanding What Happens Next, we discuss important decoupling trends, what steps global leaders will be forced to take later this year to deal with them, why these steps won’t work, and what prudent individuals should be doing now to protect themselves and their wealth.

Click here to access Part II of this report (free executive summary; enrollment required for full access).

by tictac1

by tictac1