There are three core ideas in this solo Finance U podcast (Paul was traveling at the time of recording, so it’s only me today):

- From an earlier podcast, I noted that the US is “eating the seed corn” by exporting its crude reserves and petroleum inventories to the rest of the world (presumably to try to keep prices down for a little longer).

- Commodities are both extremely undervalued and in obviously short supply, setting up a massive bull market in resources. I use copper as a fractal example of the larger thesis.

- Because of #1 and #2 above, a very large wave of inflation is on the way.

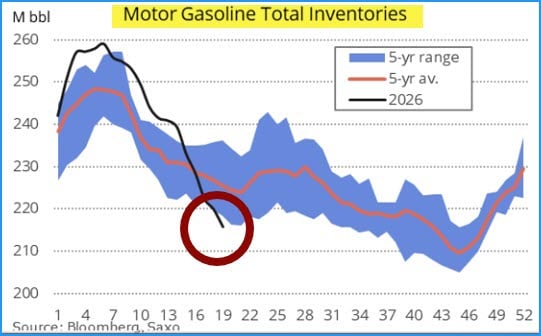

Last week (May 4th to May 8th), the US withdrew a record amount of oil from its so-called ‘strategic reserve, and exported a huge amount of gasoline, bringing its stocks to extremely low levels.

The prediction here is simple: Higher oil and gasoline prices are on the way.

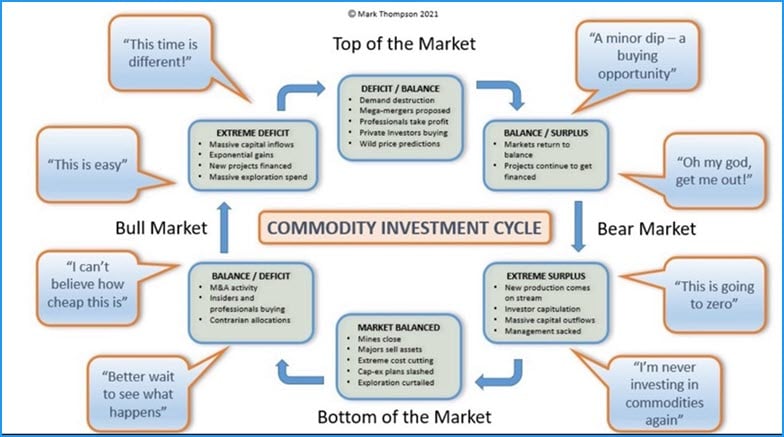

The Commodity Boom

Commodities are famous for going through cycles:

Long periods of overinvestment create surpluses and low prices, which are followed by underinvestment, deficits, and price surges.

After decades of underinvestment (especially post-2008/2010s), the market has shifted from surplus to deficit, a period when insiders and professionals quietly accumulate resources and resource equities.

The legendary copper expert and investor Robert Friedland said that if we humans want 3.5% GDP growth over the next 18 years, then we’ll have to mine more copper in that short period of time than has been mined over the last 10,000 years combined.

To really grasp this, I had to take a quick detour through exponential growth, of course. The main idea is that each exponential doubling has more in it than all the prior doublings combined.

Here’s an exponential series of doublings. 1, 2, 4, 8 ,16, 32. Note that in going from 2 to 4, the prior doubling only adds up to 3 (1+2) where the next doubling adds 4. Similarly, going from 4 to 8 gives us 7 (4 + 2 +1) in the prior doublings and 8 for the next. And on and on.

The next point Robert made was that “if we want 3.5% GDP growth,” then we’re going to fully double in just 18 years. To gut check this all we have to do is use the rule of 72. By dividing 72 by the rate of growth (3.5%) we get 72/3.5 = 20.5 years. Close enough! FYI – to get to the 18 years Robert claimed for the next doubling, the growth rate would have to be 4%.

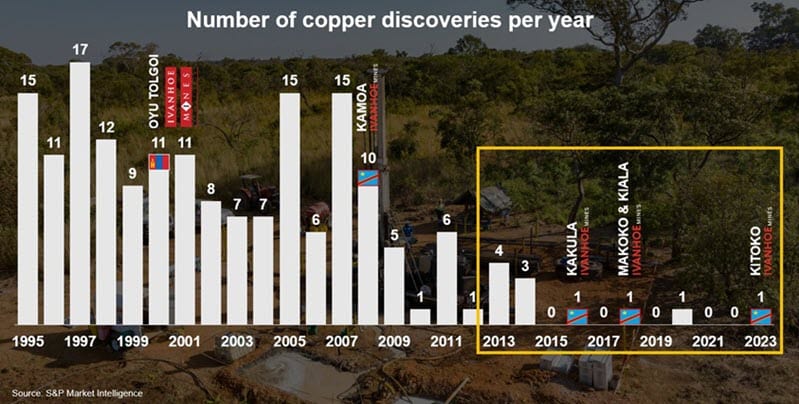

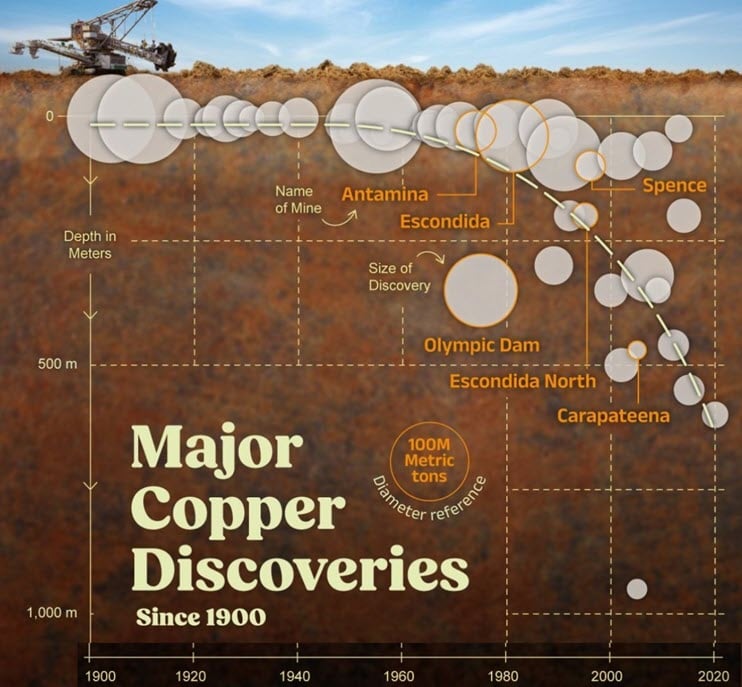

But how are ‘we’ going to enormously expand copper production? I mean, to mine it, you have to find it first, and on that front, the past ten years have been something of a disaster:

Since 2015, the world has only found four good copper discoveries, whereas Robert says we need to be finding and bringing into production six each year from here to 2050 to achieve our dreams of moving off fossil fuels.

And of the copper mines we are finding, they tend to be deeper, more dilute, and more diminutive.

There are similar stories to be told for silver, palladium and platinum to name a few other metals.

Inflation

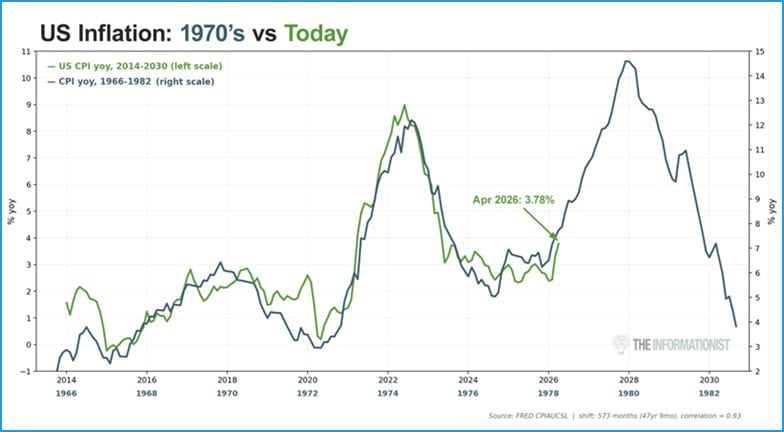

History doesn’t repeat…except when it does. This may be one of those times. The energy shock of today, coupled to the massive government deficits and a compliant and print-happy Federal Reserve, nearly perfectly mirrors the conditions of the 1970s to early 1980s when the US experienced a severe double-hump inflationary wave.

Here’s the current situation (in green) as compared to that period of time (in black):

(Source – X – James Lavish)

Oh boy. If the above chart and the commodity and energy shock come together as I suspect, then within a year or two, we’ll all be struggling with 15% to 20% inflation.

Suffice it to say, it is devilishly tricky not to lose ground as an investor during such periods of time.

Bonds are a no-no, and were called “certificates of confiscation” during the 1970’s inflationary period.

Stocks might keep pace with inflation, but may not.

Commodities and hard assets have traditionally provided some of the strongest protection against inflation in the past. Will they do this again? I suspect they will, but I don’t know.

But I do know that remaining well-informed and nimble will be more important than ever over the years to come.

Timestamps

02:58 Understanding the Commodity Cycle

06:50 The Copper Bull Market: A Deep Dive

12:03 The Supply-Demand Gap in Critical Minerals

18:06 Exponential Growth and Its Implications

26:17 Understanding Exponential Growth and Its Implications

30:40 The Impact of Food Supply on Inflation

35:01 Analyzing Precious Metals in the Commodity Super Cycle

42:34 Inflation Trends and Economic Predictions

50:53 Strategizing for a Commodity Super Cycle

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.

by cmartenson

by cmartenson