Once a quarter, I get to sit down with Adam Rozencwajg, and it’s always a treat. Adam is a Managing Partner at Goehring & Rozencwajg, a natural resources investment firm.

This was the first time I got to speak with Adam since the Iran war broke out, and the Strait of Hormuz (SoH) was effectively closed down.

The energy shock that’s underway is not just historic, but the largest in history. It’s larger than the 1973, 1979, and 20922 crises combined.

Adam tells us that the physical volumes lost are already approaching ~1 billion barrels after ~8 weeks, with the shortfall not immediately recoverable upon reopening

Despite this, market complacency is extreme. Oil has hardly reacted to the realities as compared to its movements in prior eras. But don’t worry, it will.

Adam explained that the IEA’s accounting for the alleged oil surpluses in 2025 was flawed. Where the IEA claimed there was a 2-3 million barrel per day (Mb/d) surplus throughout 2025, inventories built up minimally during that period of time. If such a surplus existed, those inventories would have shot higher by 60 to 90 Mb per month.

But now that the Strait has been closed down for just over 2 months at the time of this recording, all floating inventories have already been depleted, and onshore inventories are starting to wither away.

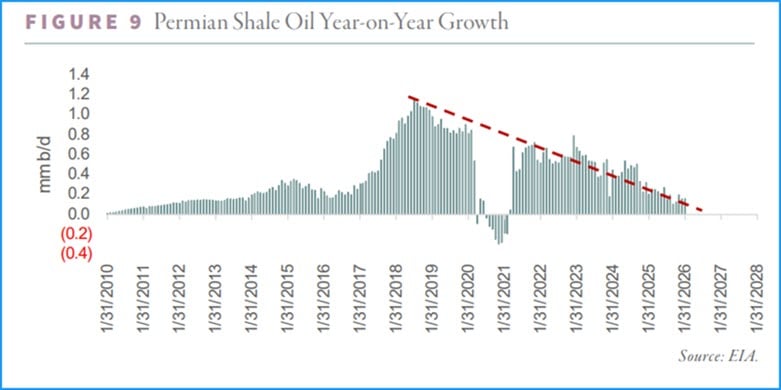

The idea that the US is going to become the world’s oil and NG producer is not supported by the facts. Adam and his team run a comprehensive neural net analysis on shale production, and their view is that US shale oil production growth is over.

In support of their model’s conclusions is this chart of the last remaining shale basin that’s shown any growth at all since 2019: the Permian.

With every passing month and year, the Permian has been offering up less and less production growth, and it will struggle to meaningfully increase its output for anything longer than brief, capital-intensive bouts.

All of this leads to the prospect of oil shortages and market black swans as sudden shortfalls and price adjustments become the mechanisms by which reality and physics assert themselves.

A short-term spot oil spike above $200 is possible due to delivery squeezes and logistical lags (tankers move slowly). Long-term, chronic underinvestment (~$500B vs. the needed $1–1.5T upstream annually) sets up a multi-year bull market.

While the crisis is exacerbating the urgency, in many ways, this is a classic resource investing bear cycle that will be followed by a bull market. Underinvestment leads to shortfalls, which lead to higher prices, which lead to more investment, which leads to oversupplies and declining prices. Up and down, over and over again.

On that basis, Goehring & Rozencwajg’s latest quarterly missive also runs a new method for calculating the degree of over- or under-investment, and commodities are about as unloved and underinvested at the moment as they ever have been in the past 100+ years.

In Adam’s view, the Strait closure is a catalyst/accelerant, but not the root cause of our energy predicament. Structural issues such as depletion, chronic underinvestment, rising marginal costs, and surging demand (especially power) point to a multi-year commodities bull market, most pronounced in oil and natural gas. Capital-starved sectors with bearish narratives embedded offer significant upside once reality sets in. Gold has already broken out; most other commodities remain early in the cycle.

Tune in to hear it all for yourself.

Timestamps

00:00 The Energy Shock: Understanding the Current Crisis

08:42 Market Complacency: The Disconnect Between Prices and Reality

14:29 The Strait of Hormuz: Implications of Closure

21:14 Shale Production: The Future of U.S. Oil Supply

32:59 Geopolitical Noise and Market Dynamics

35:40 The Future of Natural Gas

51:21 Understanding Commodity Markets and Investment Opportunities

FINANCIAL DISCLAIMER:

The information contained in this video and the resources available for download through our affiliated website are not intended as and shall not be understood or construed as financial advice, nor should be interpreted as a solicitation to sell or offer to sell investment advisory services. No person who currently works for or contracts with Peak Prosperity or Peak Financial Investing is an attorney or accountant, nor are we holding ourselves out to be, and the information contained in the video and on the website is not a substitute for legal or tax advice from a professional who is aware of the facts and circumstances of your individual situation. While Peak Financial Investing is a registered investment advisor, please note that this podcast is not intended to be investment advice.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. We have done our best to ensure that the information provided is accurate and provides what we feel is valuable information. The views expressed are subject to change based on market and other conditions.<

No guests or clients appearing on the podcast receive any form of compensation for their appearance and obtained no other benefit from either Peak Prosperity or Peak Financial Investing.

All investing involves risks including the possible loss of capital. Asset allocation and diversification does not ensure a profit or protect against loss. Please note that out- performance does not necessarily represent positive total returns for a period. There is no assurance that any investment strategy will be successful. All investments carry a certain degree of risk. Dividends are not guaranteed, and a company’s future ability to pay dividends may be limited.

Additional important disclosures for Peak Financial Investing may be found in our Form ADV Part 2A, which can be found at https://adviserinfo.sec.gov/firm/summary/319672.

by mathias_thorvik

by mathias_thorvik